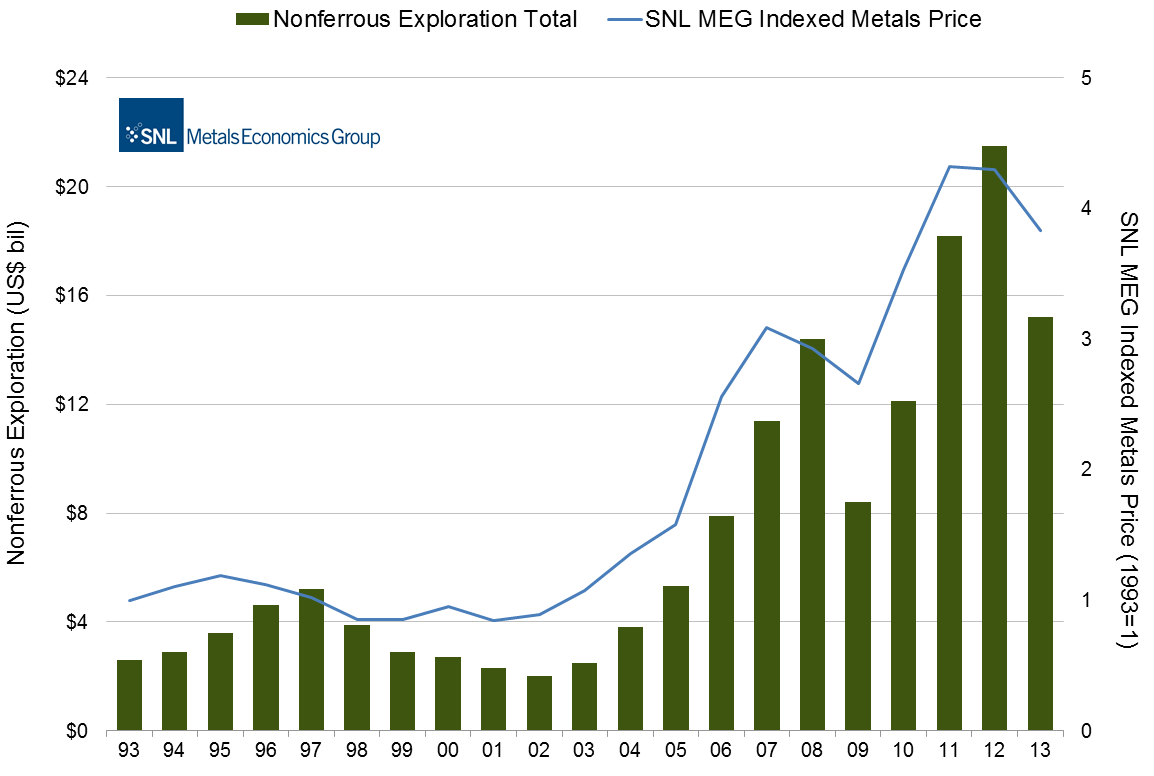

SNL Metals Economics Group’s 24th Corporate Exploration Strategies Estimates Worldwide Exploration Budgets to Fall 29% to $15.2 Billion in 2013

Halifax, Nova Scotia (PRWEB) October 24, 2013 -- SNL MEG’s 2013 exploration data and analysis are based on information collected from almost 3,500 mining and exploration companies worldwide, of which more than 2,100 had exploration budgets for 2013. The companies (each budgeting at least $100,000) budgeted a total of $14.43 billion for nonferrous exploration in 2013. Including our estimates for budgets we could not obtain, the 2013 worldwide exploration budget came to $15.2 billion. (Note: Nonferrous exploration refers to expenditures related to precious and base metals, diamonds, uranium, and some industrial minerals; it specifically excludes iron ore, aluminum, coal, and oil and gas.)

Since early 2012, junior companies have struggled to attract investor interest, and have been forced to rein in spending as their coffers become depleted; in 2013, the juniors’ total exploration budget fell 39% year on year, dropping their share of the overall total to 34% from a high of 55% in 2007. Although most metals prices remain at or near ten-year averages, higher operating and capital costs, along with pressure from activist shareholders, have required major companies to focus on a return to healthy margins after years of growth-oriented spending. The majors’ cutbacks in capital projects and exploration led to a 24% drop in their exploration budget total in 2013.

Despite lower allocations for most countries, companies continue to explore across the globe, with exploration planned for 127 countries in 2013, down from 129 in 2012. This includes a continued willingness to explore in high- or medium-risk jurisdictions, which accounted for more than half the annual budget total for the past several years, despite ongoing concerns and uncertainty over security, policy, taxation, and resource nationalism. In contrast, the share of budgets allocated to mature mining regions such as Canada and the United States fell in 2013: Canada’s total budget was down 41% year on year due to weakness in the country’s junior sector, while the United States’ total declined 38% as many gold majors scaled back exploration programs. Canada and Australia remained the top countries overall, with the United States, Mexico, and Chile rounding out the top five.

The proportion of overall exploration budgets dedicated to minesite work reached a new historical high in 2013, with producers emphasizing brownfields programs as a less capital-intensive and less risky means of replacing and adding reserves. In contrast, many junior companies sharply curtailed late-stage and feasibility programs in an effort to conserve cash, while some majors made strategic decisions to scale back late-stage exploration due to near- and medium-term uncertainty. With many companies facing tough financial and strategic choices, the pool of early- and late-stage assets available for sale is likely near an all-time high—a situation yet to be taken advantage of by potential buyers, such as mid-tier producers, new industry entrants, or companies based in emerging economies.

Christina Twomey, SNL Financial, http://www.SNL.com/AsiaPacBanks, +1 434 951 6914, [email protected]

Share this article