Student Debt Infographic Reveals Problems and Solutions to Rising Student Debt

Carlsbad, CA (PRWEB) September 10, 2013 -- US Student Loan Services, Inc. specializes in helping those with student loan debt by assisting them with student loan consolidation programs designed to help with their current financial situation. To further educate the public on the student debt crisis and solutions available, USSLS has created an infographic displaying how far-reaching the student debt crisis is, as well as some available solutions to ease the financial burden of student debt that has affected several generations.

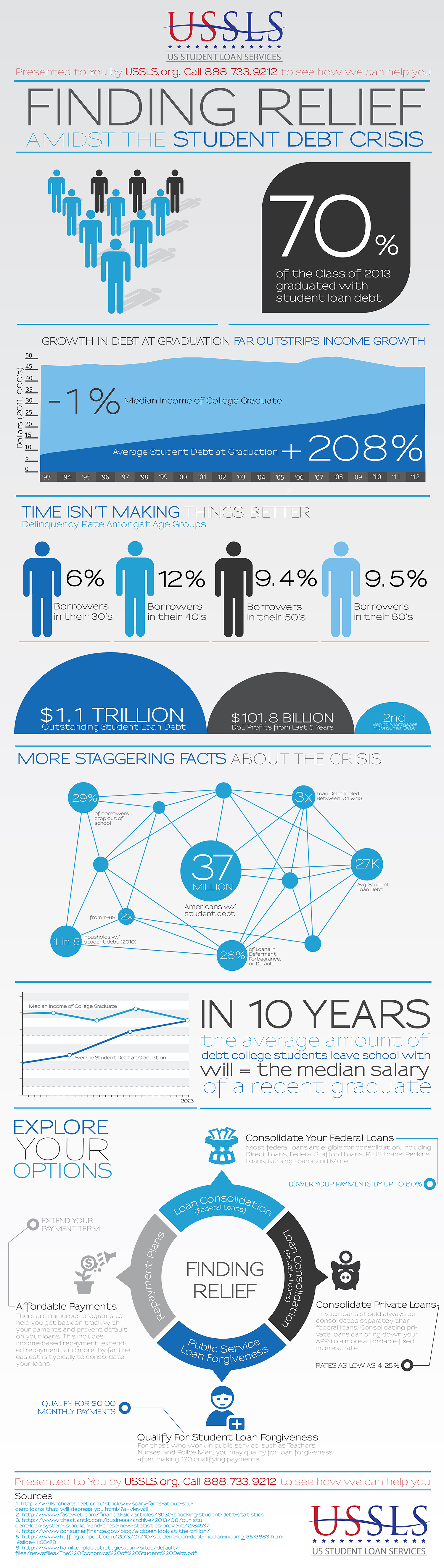

View the infographic here: http://www.usstudentloanconsolidation.org/student-loan-consolidation/infographic-finding-relief-amidst-the-student-debt-crisis/

As of March 2012, the student loan debt bubble surpassed the $1 Trillion dollar mark. Put into perspective, the student loan debt in the United States has climbed beyond credit card debt for the first time in history and is second only to mortgage debt.

It is not surprising then to know that the average amount of debt one has after college is just over $27,000. For a student attending graduate school or pursuing a PhD, it is not uncommon to leave school with more than $100K in student debt.

It’s not just the students who have been burdened by the high-cost of attending college, but also parents, and in some cases, grandparents. Take for instance the delinquency rate (more than 60 days late on payments) amongst various generations. For borrowers in their 30’s that number is 6%. For those in their 50’s, it is 9.4%. For borrowers in their 60’s, it is slightly higher at 9.5%. And for borrowers in their 40’s, the number is double that of those in their 30’s at 12%.

The job market in the United States certainly does not help the matter. In a recent Forbes article (June 2013), the unemployment/underemployment rate was cited as being 14.3%. It is no wonder then that these age groups are facing high delinquency rates.

Along with the lack of jobs and high student debt amounts comes the cutting off of disposable income and inability to qualify for long-term finance purchases, such as a house or a car. Recently, a study found roughly 22% of 30-year-olds with a history of student debt owed money on a mortgage, compared to 24% of 30-year-olds who never took out a student loan. Traditionally, the percentage of homeowners who have student debt has still been higher due to their ability to find a higher paying job. It is estimated that for every $100/month you owe on educational debt, it subtracts $20,000 from the price of a home you can afford.

These debt burdens have even permeated into relationships. A growing trend is developing among younger generations who put off getting married, or even dating, due to their large debt load. For many, it is embarrassing and discourages the hope of “settling down” and starting a family any time soon. Paying off the monthly tab for their loans becomes the sole focus, leaving little for disposable income after the bi-weekly paycheck rolls in.

Much of these problems: the loans in default, lack of home buying, and intrusion of personal life, often comes down to a lack of understanding about one’s options for repaying their student loan debt.

“We see it all the time: people approach us simply looking for help and are amazed at the options available out there,” says one of the senior counselors of US Student Loan Services. “Most people are willing to pay something, they just need someone who can properly educate them and walk them through the process. That’s where USSLS comes in. We work to help borrowers identify what programs are available and then complete the necessary steps to qualify them into those programs.”

USSLS (http://www.USSLS.org) works with student loan borrowers to qualify them for existing programs which for many, may reduce monthly payment, provide a better average interest rate, increase their financial profile and may even include loan forgiveness. The end result, “People are quite pleased once they find out their new monthly payment. They just want some breathing room, and that’s what we strive to help them find.”

USSLS also specializes in setting up those who qualify into Loan Forgiveness Programs. These are available for those who work in public service jobs, such as teachers, some nurses, non-profit employees and government employees. After 120 qualifying payments, the rest of the debt amount may be forgiven under this program. “Ultimately, we hope to get the word out about these different programs that are available and provide some relief to those climbing the mountain of paying back student debt,” reports USSLS.

US Student Loan Services was founded in 2012 by Jerry McTaggart, founder of Christian Credit Counselors and a prominent leader in the credit counseling industry since 1962. USSLS helps those facing student loan debts by identifying what programs are available to help them and then providing the services to complete the process of qualification for the best program.

You can view the infographic at http://www.usstudentloanconsolidation.org/student-loan-consolidation/infographic-finding-relief-amidst-the-student-debt-crisis/ or visit their site at http://www.USSLS.org.

Public Relations, USSLS, http://usstudentloanconsolidation.org, +1 (888) 733-9212, [email protected]

Share this article