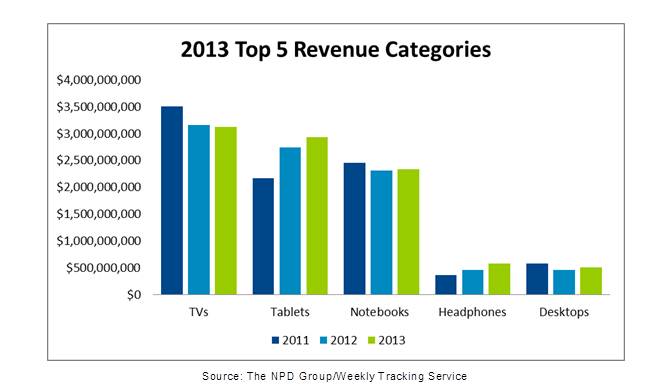

Key CE Categories Deliver Positive 2013 Holiday Results, According to NPD

Las Vegas, Nevada (PRWEB) January 07, 2014 -- The top five U.S. CE* categories by revenue; desktops and notebook PCs, TVs, tablets and headphones collectively delivered $1.3 billion more in additional industry revenue this holiday** season than they did just four years ago, according to The NPD Group’s Weekly Tracking Service***. Revenue for these categories was almost $9.5 billion in 2013, up 3.7 percent on top of last year’s 1 percent increase. Every one of these categories also delivered at least a flat unit volume performance versus 2012 led by the 45 percent unit increase in tablet sales.

“This was a unique calendar year; with Thanksgiving coming so late, the importance of the early selling season was amplified,” said Stephen Baker, vice president, industry analysis, The NPD Group. “It is not a coincidence that four of these product groups were among the most highly promoted products during Black Friday and Cyber Week promotions.”

Sales were especially strong during the first three weeks of the 2013 holiday season. Thanks to a strong Thanksgiving week, and positive sales momentum during Cyber Monday week, revenue reached nearly $10.5 billion, an increase of 6.6 percent versus the same time period in 2012. Additionally, the U.S. experienced the strongest pre-holiday sales in two years, with early November sales increasing 5.6 percent over 2012.

TVs remained the largest revenue category and had a surprisingly strong holiday season, up 4 percent in units after close to a full year of monthly unit volume declines. Despite the highly-promotional early holiday season, overall TV average selling prices (ASPs) declined by less in 2013 than in any of the previous three years, bolstered by a 55 percent increase in unit sales of TVs 60 inches and larger.

Consumers purchased 11 million tablets this holiday season, up 45 percent from 2012, but revenue only increased 7 percent. Sales of 7-inch tablets increased by nearly 2.5 million units and accounted for 38 percent of all sales, with an ASP of $102.

According to NPD, notebook PC sales were expected to experience unit and dollar declines, but they were actually flat compared with 2012. Strong unit volumes in both Macbooks (up 13 percent) and Chromebooks (up 112 percent) offset weakness in Windows devices (down 6 percent). Windows notebook ASPs, however, increased $5 this year, buoyed by touchscreen notebooks, which accounted for 38 percent of sales volumes with a nearly 10 percent price premium.

Revenue outside the top five categories fell 4.3% on top of an over 9% decline in 2012. Despite this decline a number of secondary categories had strong revenue growth and breakout sales volumes in 2013.

Most audio products continued their positive sales momentum in addition to the stellar headphone results. Sound bar sales increased nearly two times in both unit and dollar volumes, and topped $200 million in revenue for the first time. Streaming audio speakers were the star of the market this year, as revenue increased to $310 million, up 2.5 times from last year.

The accessory market was also a holiday highlight. Compared to 2012, cell phone accessory revenue topped $423 million, an increase of 17 percent. Tablet accessories also showed accelerating revenue growth, with this year’s increase of 19 percent exceeding last year’s results.

“All in all, we believe that the 2013 holiday season will be a catalyst for strong results in 2014,” said Baker. “We have a broad and deep selection of product segments showing unit and dollar growth. These fundamental, positive trends, combined with what is likely to be a strong year for new product introductions, point to an encouraging outlook for 2014.”

*Consumer electronics excludes mobile phone, Kindle, and video game hardware and software sales.

**Five week 2013 holiday includes sales from November 24, 2013 – December 28, 2013.

***NPD’s weekly POS information is derived from a subset panel of retailers that also contribute to NPD’s projected monthly POS panel.

About The NPD Group, Inc.

The NPD Group provides global information and advisory services to drive better business decisions. By combining unique data assets with unmatched industry expertise, we help our clients track their markets, understand consumers, and drive profitable growth. Sectors covered include automotive, beauty, consumer electronics, entertainment, fashion, food / foodservice, home, luxury, mobile, office supplies, sports, technology, toys, and video games. For more information, visit http://www.npd.com and npdgroupblog.com. Follow us on Twitter: @npdtech and @npdgroup.

Sarah Bogaty, The NPD Group, http://www.npd.com, 516-625-2357, [email protected]

Share this article