Public Cloud Leaders Enlist ISV and C&SI Partners to Sustain Market Positions and Sell Horizontal Clouds in Vertical Markets

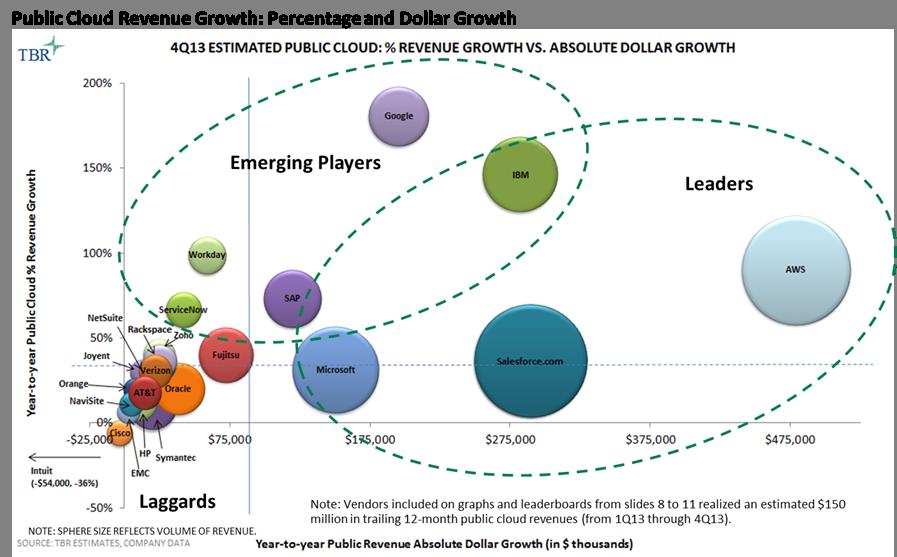

Hampton, NH (PRWEB) April 28, 2014 -- According to Technology Business Research Inc.’s (TBR) 4Q13 Public Cloud Benchmark, public cloud* revenue grew 47.4% from the year-ago quarter to $6.2 billion across the 50 vendors covered in the report, while market growth for overall public cloud services grew 25.6% year-to-year over the same period to $15.1 billion. Cost savings, interoperability, ease of use, and the overall acceptance of public cloud across the vendor and customer landscape drove growth.

“With the acquisition landscape relatively quiet over the past six months, leading public cloud vendors are evolving go-to-market strategies to embrace ecosystem-led approaches that are needed to increase reach and serve the broadest markets,” said Jillian Mirandi, senior analyst for TBR’s Cloud Practice. “A large and diverse ISV partner base will help tailor products vertically and horizontally, increasing vendors’ stickiness, while C&SI alliances help create new use cases and improve overall value propositions.”

For example, SaaS leaders such as Salesforce.com and Box are increasingly relying on the channel to tailor core solutions to verticals, while IaaS leaders such as Amazon Web Services (AWS) and Google are expanding C&SI alliances to improve their high-touch consulting, integration, migration and customization services to meet enterprise customers’ demands.

To expand reach within customer bases and improve sales and marketing strategies, public cloud leaders across cloud segments (i.e., SaaS, PaaS, IaaS) will prioritize investments in emerging BI, analytics and big data use cases in 2014. While vendors such as ServiceNow and Box internally use customer analytics to quickly address customer issues, mitigate potential renewal threats, and unearth best-in-class upselling and cross-selling strategies, portfolio investments to offer these capabilities to customers will help vendors differentiate and capture the next wave of public cloud demand. In particular, nearly every public IaaS vendors including GoGrid, Microsoft, Rackspace and AWS has invested in technological collaborations with BI, Hadoop and NoSQL database providers to optimize IaaS portfolios for running and analyzing big data workloads in the cloud. In the PaaS space vendors are opening APIs — IBM for Watson and HP for Vertica and Autonomy — to enable developers to add BI and analytics capabilities to applications.

Large IT vendors will drive public cloud consolidation through acquisitions in 2014 to fill capability gaps and expand regionally and vertically. TBR expects IBM to follow its February acquisition of Database as a Service provider Cloudant with additional niche vendor acquisitions to expand cloud-centric engagements with customers and minimize install base attrition. Additionally, HP and Cisco are expected to make notable public cloud acquisitions of hybrid integration, cloud management and IaaS vendors to complement their large, multicloud businesses.

TBR’s Cloud Practice provides syndicated report coverage of 23 vendors, and its Public Cloud Benchmark, Managed Private & Professional Services Cloud Benchmark and Cloud Components Benchmark cover 50, 29 and 11 vendors, respectively. The practice also offers customer research and satisfaction studies that identify vendor performance relating to customer perception.

On April 15 at 1 p.m. EDT TBR Principal Analyst Allan Krans and Senior Analyst Jillian Mirandi will present additional details of public cloud vendor performance, market trajectory and business model analysis in a webinar, State of the Public Cloud Market — Insights from TBR’s Public Cloud Benchmark. To register, visit http://tbrevents.webex.com.

For more information about TBR’s public cloud research or entire cloud research portfolio, please contact Alison Crawford, senior marketing manager, at 603.758.1838 or alison.crawford(at)tbri(dot)com, or James McIlroy, vice president of Sales, at 603.929.1166 or mcilroy(at)tbri(dot)com.

*Public cloud includes Software as a Service (SaaS), Platform as a Service (PaaS) and Infrastructure as a Service (IaaS) along with all relevant subcomponents. Public cloud market growth is based on the 50 vendors included in TBR’s Public Cloud Benchmark coverage. The growth rates represent quarterly comparisons between 4Q13 and 4Q12.

ABOUT TBR

Technology Business Research, Inc. is a leading independent technology market research and consulting firm specializing in the business and financial analyses of hardware, software, professional services, telecom and enterprise network vendors, and operators. Serving a global clientele, TBR provides timely and actionable market research and business intelligence in a format that is uniquely tailored to clients’ needs. Our analysts are available to further address client-specific issues or information needs on an inquiry or proprietary consulting basis.

TBR has been empowering corporate decision makers since 1996. For more information please visit http://www.tbri.com.

Alison Crawford, Technology Business Research, Inc., http://www.tbri.com, +1 7814209497, [email protected]

Share this article