LCD TV Growth Improving, As Plasma and CRT TV Disappear, According to NPD DisplaySearch

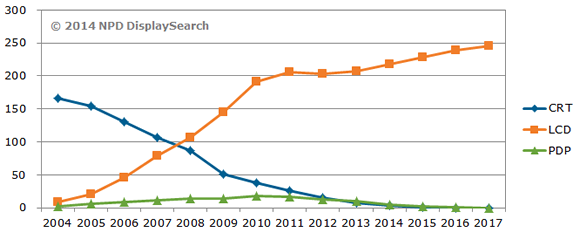

Santa Clara, Calif. (PRWEB) April 16, 2014 -- Since reaching a peak in 2011, the global TV market has seen continuous declines, falling by 6 percent in 2012 and by 3 percent in 2013. LCD TV shipment growth fell into single digits in 2011, experienced its first decline in 2012, and grew by only 2 percent in 2013, which was not enough to make up for falling shipments of plasma and CRT TVs. According to NPD DisplaySearch, with LCD passing 90 percent of global TV shipments, it is the dominant driver of industry growth.

According to the latest TV market forecast published in the NPD DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report, worldwide TV shipments are projected grow by less than 1 percent in 2014, but LCD TV units will rise almost 5 percent. Of course, the growth of LCD comes at the expense of plasma and CRT TV shipments, which are forecast to fall 48 percent and 50 percent, respectively, in 2014. In fact, both technologies will all but disappear by the end of 2015, as manufacturers cut production of both technologies in order to focus on LCD, which has become more competitive from a cost standpoint. OLED is also expected to grow as an alternative flat panel display technology for TVs, but is expected account for less than 1 percent of units through 2017.

“TV shipments worldwide have struggled for the past several years, as several unusual events have disrupted normal buying patterns,” according to Paul Gagnon, director for global TV research at NPD DisplaySearch. “Governments instituted subsidy programs to prop up local economies in the post-recession years from 2009 through 2013, and digital-to-analog broadcast transitions for many developed and emerging countries accelerated demand for TVs further, at the expense of future demand.”

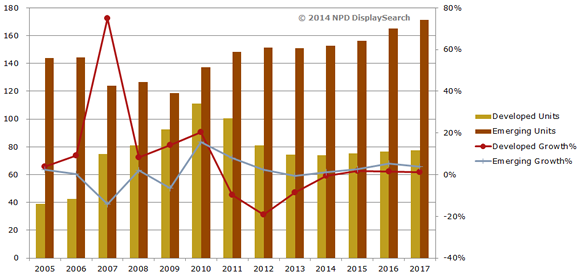

Developed Region Growth Stabilizes, While Emerging Region Growth Remains Soft

The collective emerging regions of the world have long dominated global TV demand; however, at the end of the last decade, TV demand growth surged in developed regions, which included Japan, Western Europe and North America. Much of this increased growth rate was due to analog broadcast shut-off events, as well as rapid cost reductions on flat panel TVs. Japan and other governments also implemented spending programs, to boost local demand for energy-efficient TVs and other products. Since then, shipments have declined significantly, as future demand was satisfied during the boom years, though demand has stabilized around 75 million units annually.

Meanwhile, emerging region growth accelerated from 2009 through 2012, as demand from China skyrocketed, due to several local subsidy programs. With the China subsidy program now ended, and CRT demand falling more quickly than LCD can grow in Asia Pacific and other regions, growth factors have turned distinctly weaker for emerging regions. The World Cup in 2014 and Summer Olympics in 2016, both of which occur in Brazil, will likely have a stimulus effect in many emerging countries. Finally, the end of CRT TV availability will transition purchasing behavior to flat panel TVs.

The DisplaySearch Q1’14 Quarterly Advanced Global TV Shipment and Forecast Report, available now, includes panel and TV shipments by region and by size for nearly 60 brands, and also includes rolling 16-quarter forecasts, TV cost/price forecasts and design wins. For more information about the report, please contact Charles Camaroto at 888-436-7673 or 516-625-2452, e-mail contact(at)displaysearch(dot)com, or contact your regional NPD DisplaySearch office in China, Japan, Korea or Taiwan.

About NPD DisplaySearch

NPD DisplaySearch, part of The NPD Group, provides global market research and consulting specializing in the display supply chain, including trend information, forecasts and analyses developed by a global team of experienced analysts with extensive industry knowledge. NPD DisplaySearch supply chain expertise complements sell-through information from The NPD Group, thereby providing a true end-to-end view of the display supply chain from materials and components to shipments of electronic devices with displays to sales of major consumer and commercial channels. For more information, visit us at http://www.displaysearch.com. Read our blog at http://www.displaysearchblog.com and follow us on Twitter at @DisplaySearch.

About The NPD Group, Inc.

The NPD Group provides global information and advisory services to drive better business decisions. By combining unique data assets with unmatched industry expertise, we help our clients track their markets, understand consumers, and drive profitable growth. Practice areas include automotive, beauty, consumer electronics, entertainment, fashion, food/foodservice, home, luxury, mobile, office supplies, sports, technology, toys, and video games. For more information, visit npd.com and npdgroupblog.com. Follow us on Twitter at @npdtech and @npdgroup.

Lee Graham, The NPD Group, 212-333-4983, [email protected]

Share this article