Mortgage Elements Expands Database to Include Correspondent Lenders

Chicago, IL (PRWEB) May 28, 2014 -- Mortgage Elements started out as a tool to help Mortgage Brokers find Wholesale Lenders and research their different loan programs. But as the Consumer Finance Protection Bureau (CFPB) rolled out the Qualified Mortgage rules (QM) on January 10 of this year, many Brokers supplemented or switched their loan originations to the Correspondent Lending channel. This coincides with many large Mortgage Lenders such as Wells Fargo, Fifth Third, Everbank, NationStar, and Suntrust that have closed their Wholesale Mortgage divisions in 2013 and shifted their resources to the Correspondent Lending channel. Along with existing Mortgage Lenders shifting resources to Correspondent Lending, many new entrants have opened Correspondent Lending divisions.

Wholesale and Correspondent lending is collectively referred to as "Third Party Origination" or TPO lending because the loan is originated by a third party like a Mortgage Broker or Mortgage Banker. The main difference between the two channels is the source of the funds to close the loan. In the Wholesale Mortgage channel, the funds used to close a loan is provided by the Wholesale Lender at the closing table. This is called "table funding". The Mortgage Broker who originated the loan does not use any of their own funds. In the Correspondent Mortgage channel, the funds to close a loan is provided by the Mortgage Banker that originates the mortgage. The Mortgage Banker then sells the closed loan to the Correspondent Lender and the Mortgage Banker is reimbursed the funds they used at the closing table.

When a Mortgage Broker migrates from the Wholesale Lending channel to the Correspondent Lending channel they become a "Mortgage Banker". Becoming a Mortgage Banker requires a higher net worth, more regulatory scrutiny, is much more work, and carries higher risks. For many Mortgage Brokers, this is just a natural part of their long term growth plans, but other Brokers have become Mortgage Bankers in response to the new regulations.

The addition of Correspondent Lenders to its database is a natural progression for Mortgage Elements. Mortgage Elements is a tool designed to help Mortgage Professionals find and research different loan programs being offered by various Wholesale and Correspondent lenders throughout the country. The website helps lending professionals quickly navigate through an ocean of data to find relevant mortgage information.

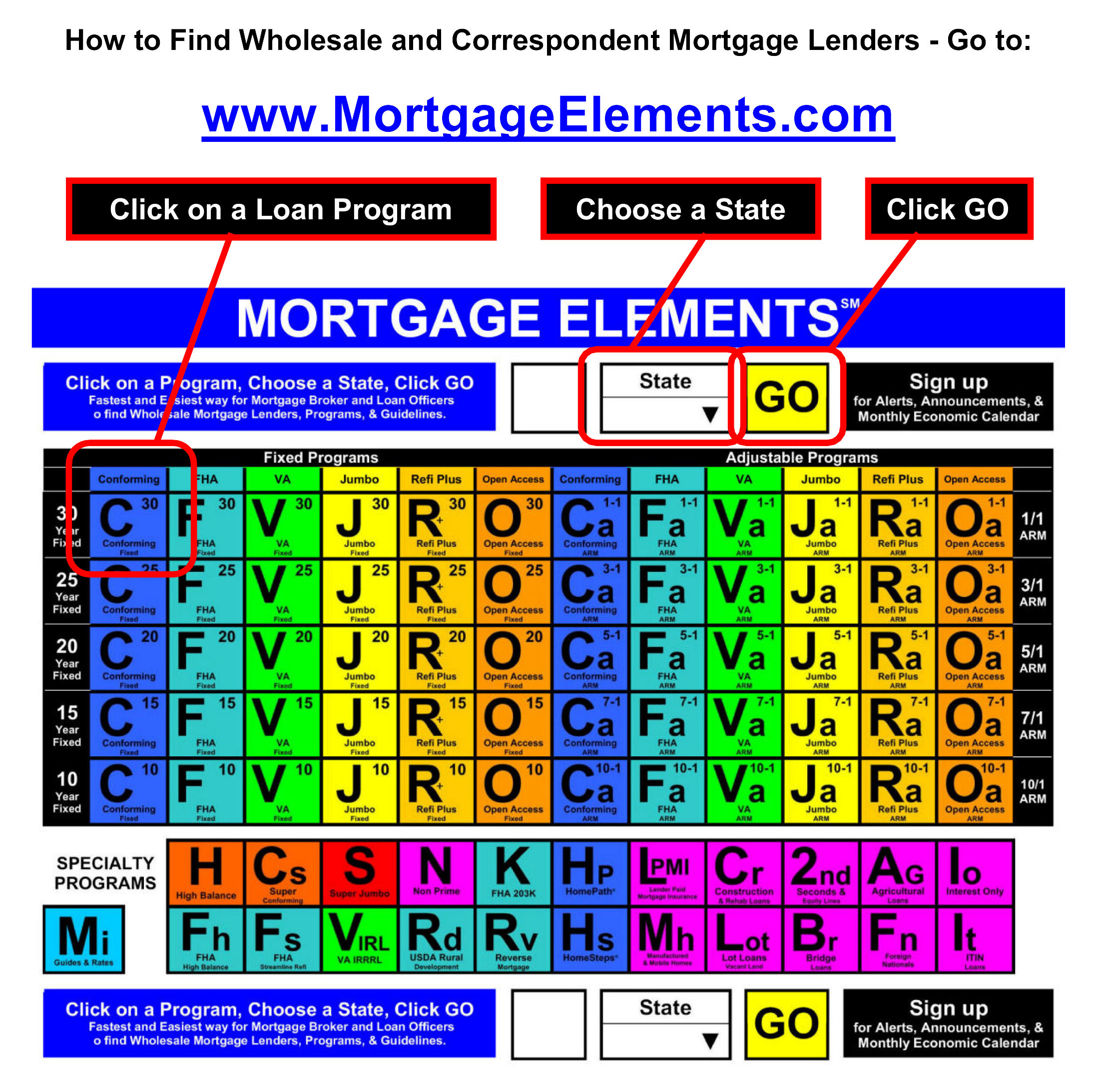

The website and database are free for use by all Mortgage Professionals with no registration or subscription fee required. Listing in the database is also free for all Wholesale and Correspondent lenders. The database is accessed through the Mortgage Elements homepage at http://www.MortgageElements.com by using a unique graphic interface - a Periodic Table of Mortgage Programs. This design enables the user to quickly find lenders and loan programs from a desktop computer, iPad/tablet, or smartphone - all it takes is a few mouse clicks or taps on the screen. The website contains links to different Wholesale/Correspondent lenders' websites which helps to research the various loan programs.

About Mortgage Elements Inc.

Mortgage Elements Inc. is an internet marketing company that provides marketing, database, search, and consulting solutions for the mortgage industry through its website http://www.MortgageElements.com. The company uses a unique website design optimized for touch screen technology and use on mobile devices, desktop, and laptop computers. Mortgage Elements is a B2B company for the mortgage industry and not a lender.

Mark Paoletti, Mortgage Elements Inc., http://www.MortgageElements.com, 630-529-3755, [email protected]

Share this article