Testing the waters for offshore treatment

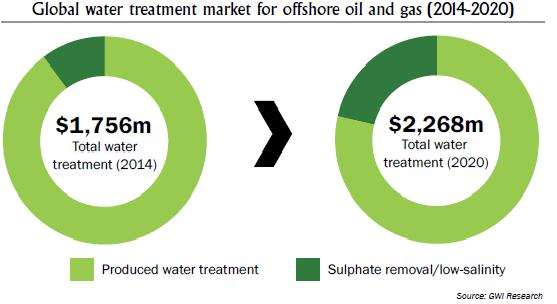

(PRWEB) October 27, 2014 -- The market for spending on water treatment in the offshore oil and gas industry is set to grow by an annual average of 4.4% in the next six years, driven by increasing production from developing markets around the world, and the need for more advanced solutions to keep mature oilfields productive. Today, the offshore oil and gas industry accounts for approximately 27% of worldwide production. The choice of water treatment technology is becoming increasingly important where production challenges are higher: in ultra-deep waters, enhanced oil recovery projects and mature fields with high volumes of produced water. In 2014, the global market for water treatment solutions for the offshore oil and gas industry is estimated to be worth $1.76 billion (see chart).

Separating oil from water

Water treatment systems used on offshore facilities have to adhere to restrictions on size and weight, making design and engineering far more complex and capital-intensive than is the case in the onshore industry. These restrictions pose a challenge when planning a facility that will handle increasing volumes of produced water, which are expected to reach 43 million barrels per day globally in the offshore sector by 2020.

In 2013, 84% of global offshore produced water was managed by treating it prior to overboard discharge, while 14% was reinjected and the remaining 2% was disposed of in onshore deep wells. Produced water treatment, which is dominated by oil/water separation equipment in the offshore industry, represents the largest share of the water treatment market, worth $1.58 billion in 2014. Global Water Intelligence anticipates that the market will grow by a CAGR of 2.1% until 2020.

Low salinity, high expectations

Membrane technologies have found a niche in the offshore oil and gas industry, driven by the need to ensure that injected seawater is compatible with water in hydrocarbon-bearing formations.

The report shows that, since 2000, 1.7 million m3/d of desalination capacity has been installed for sulphate removal systems worldwide. These technologies are most prevalent in the deepwater fields of the Atlantic rim, where the threat of disruption by scale formation encourages their adoption by facility operators. The market for membrane-based treatment systems for water injection is expected to see an impressive CAGR of 18%, creating a market worth $480 million in 2020.

Global drivers

Capital expenditure on water treatment equipment is expected to show steady growth of 4.4% a year to reach $2.27 billion in 2020. There are three primary drivers of spending on water treatment in this industry:

• Demand for sustained oil and gas production – exploration and production companies want to maintain their revenues from oil and gas production, particularly national oil companies, which typically have assets focused in a single region. Sulphate removal treatment reduces the chance of plugging the well and suspending production. Furthermore, the application of EOR methods that require membrane- based treatment could increase the volume of oil that can be recovered.

• An increase in produced water volumes – similar to the onshore industry, maturing offshore oil fields are generating increasing volumes of produced water compared to oil production. If these fields are to stay online, they will require investment to upgrade existing separation and treatment systems to accommodate the increase in volumes. Also, offshore facilities that are currently operating without treatment systems will have to install them when water is extracted in significant volumes.

• Limited availability of space – due to limited space on platforms or topsides on floating production, storage and offloading (FPSO) vessels, separation equipment must be more compact than onshore. It is therefore more common to make use of technologies with smaller physical footprints, such as hydrocyclones and compact flotation units, and technologies that replace several steps in the treatment train. In the long run, these limitations may encourage subsea separation systems near the wellhead.

The global view

In terms of growth, Global Water Intelligence identifies that the most attractive regional markets will be in areas that can expect to see significant investment in offshore field developments, such as the Caspian Sea. An even more attractive prospect is those regions on the Atlantic rim where the threat of scaling in deepwater wells requires the use of sulphate removal processes. Reflecting this, the GWI report envisages that Brazil and West Africa will see the fastest growth in capital expenditure.

The GWI primary research report

Water for Offshore Oil & Gas: Opportunities in sulphate removal, produced water treatment and deepwater operations - available now, priced at £2,200/$4,000. For details on how to order or to request a review copy, contact Edyta Bednorz eb(at)globalwaterintel(dot)com.

Edyta Bednorz, Global Water Intelligence, http://www.globalwaterintel.com, +44 1865204208, [email protected]

Share this article