Kline’s March Index of Base Stock Production and Re-refining Cash Margins Reflects Improved Profitability Driven by Declining Crude Oil Prices

Parsippany, NJ, (PRWEB UK) 17 March 2015 -- In January 2014,Kline & Company, a worldwide consulting and research firm serving needs of organizations in the lubricants and base stocks industry, introduced its monthly Base Stock Margin Index, a characterization of recent cash margin contributions in the U.S. base oil market over the past 24 months.

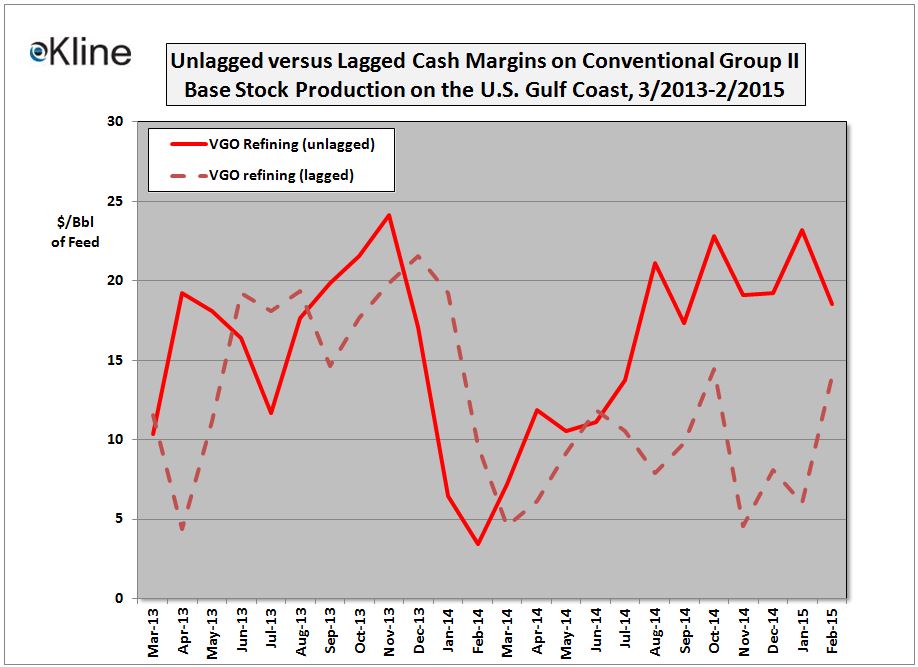

The Index estimates cash margin contributions associated with U.S. Group II base stock production. It simulates EBITDA before the deduction of corporate SG&A expenses for typical VGO-based virgin base stock plants and RFO-based re-refineries. A more detailed description of the Margin Index can be found in the January 2014 release.

Click here to view the March 2015 Index

“Crude oil prices rebounded in February, with Brent averaging $58 per barrel, which had a negative impact on instantaneous Group II cash margins,” noted Ian Moncrieff, Vice President of Kline’s Energy Practice. “With crude oil and VGO prices increasing from January lows, and Motiva’s base stock postings unchanged for the past two months, unlagged margins began to be squeezed. Although Brent crude oil has continued to firm somewhat through early March, to around $60/Bbl, overcapacity is still restraining industry-wide attempts to raise postings, with Chevron as the lone exception in announcing 20 cent/gallon increases effective March 11. The inherent lag between feedstock and base oil price movements has produced widely divergent estimates of cash margins between instantaneous and lagged results over the past six months, as crude oil and VGO prices fell faster than base oils. That disparity is much closer to being rectified, as noted in the figure below. However, industry fundamentals suggest a lower level of margin equilibrium once markets and pricing have reached a more stable basis of operations.”

For more information on the Kline Index, or to inquire about our pricing and margin analysis services to the base stocks industry, please contact Ian Moncrieff, Vice President (Ian.Moncrieff(at)klinegroup.com) at (973)-615-3680 in Kline’s Energy Practice.

About Kline & Company

Kline is a worldwide consulting and research firm dedicated to providing the kind of insight and knowledge that helps companies find a clear path to success. The firm has served the management consulting and market research needs of organizations in the agrochemicals, chemicals, materials, energy, life sciences, and consumer products industries for over 50 years. For more information, visit http://www.KlineGroup.com.

###

For more information contact:

Eric Pimenta

Marketing Communications

(973) 435-3435

Eric.Pimenta(at)klinegroup.com

Vera Sandarova, Kline & Company, Inc., http://www.klinegroup.com, +420 722-018-881, [email protected]

Share this article