South Norwalk, CT (PRWEB) July 20, 2016 -- Convergence Inc. has released a full survey report to institutional investors based on its recently completed Operations Due Diligence (ODD) Effectiveness Study. The study included institutional investor participants responsible for over $700 billion of assets under management and allocated to external managers, including allocations to both hedge fund and private equity managers. 57% of participants reported having allocations to over 50 external managers. Survey participants included a cross section of fund of funds managers, public and private pension plans, endowments and outsourced chief investment officer organizations.

Survey findings suggest that a significant number of institutional investors rely upon periodic manager communication and loosely defined processes to stay abreast of material events at advisors with investment allocations. Convergence data indicates that managers of private funds file updated regulatory filings approximately 3 times per year on average for material events impacting their business and product profile. Institutional investors may have limited resources available to pro-actively fulfill their fiduciary responsibilities in an environment of increasing regulatory scrutiny and increasing operations-related complexity.

Selected highlights and results of the study include the following:

1. Many institutional investors do not have written policies with respect to operations due diligence (ODD).

Almost 40% of institutional investors who participated in the ODD survey report NOT having written ODD policies, including as part of their overall investment policies. Beyond performance and portfolio risk, operations-related risk and controls around managing regulatory risk should be significant considerations for allocators, and warrant a documented approach to reviewing such matters.

2. Dedicated investor resources to ODD activities are not adequate to address the post-investment monitoring of operations-related risk.

A significant majority (83%) of institutional investor respondents to the survey report only having 0-3 staff resources dedicated to ODD activities. In many follow on conversations with these survey participants, even the largest institutional investors have limited dedicated resources. In certain instances, internal staff resources may be augmented with external ODD service providers and/or technology tools. However, just 23% of institutional investors report outsourcing select ODD activities.

3. Service provider assessment and ongoing monitoring by institutional investors is not sufficient given the critical nature of those relationships to the control and operations-related environment of managers.

The top 3 vendor relationships of institutional investor focus include fund administrators, auditors and custodians. A full 89% of ODD survey participants cited fund administrators in their top 3, and complete a formal verification process to ascertain that vendor relationship. Institutional investors place significant reliance on SSAE No. 16 Reports and on vendor discussions to assess the quality and fit of the vendor relative to the needs to the manager. A full 55% of institutional investors cite a change in vendors as a material event or “red flag” in conjunction with their ongoing ODD processes.

4. Institutional investors should develop and incorporate a formal manager “scoring” process, including consideration of data-driven “peer” level benchmarking, into their ODD processes.

Approximately 53% of institutional investor respondents to the survey report they incorporate a manager “scoring” process into their initial ODD evaluation. This can be in the form of a “high, medium, low”, or 1-10 scoring scale rating with respect to matters of operational infrastructure and risk, following completion of initial ODD. About the same percentage of respondents report they incorporate peer level benchmarking into their ODD evaluation process. Much of this “benchmarking” is based on anecdotal data references, comparisons to other managers across the investor’s existing allocations and based on industry intelligence.

5. Given manager expansion into new product and distribution channels and a dynamic regulatory environment, institutional investor processes for ongoing ODD need to be re-examined.

Following initial ODD and the on-boarding of a manager, the intervals and practices for follow on, or “ongoing ODD” varies significantly, particularly based on allocation fund type (hedge funds v private equity). About 63% of institutional investor respondents to the survey report performing ongoing manager reviews (absent an interim “material event”) within a 24 month interval for hedge fund allocations, while just 24% report doing so for PE allocations. The top 4 practices in place by investors as part of their ongoing ODD include 1. Review of audited financials; 2. Monitoring industry news; 3. Review of ADV filings for changes; and 4. Review of fund administrator transparency reports. Only 21% of investors in the survey report using technology-based tools in their ongoing ODD processes.

The Appendix below and attachments include the results of two select questions from the Convergence ODD study pertaining to the professional expertise of dedicated ODD staff and the primary areas of focus in investor ODD practices.

PARTNERING WITH CONVERGENCE

Convergence focuses on providing Pension – Endowments and Foundations with the information they need to identify and manage risks that are changing in their Advisor's business – INDEPENDENT of the Advisor.

Convergence enables its institutional investor clients to increase internal efficiencies, reduce third party consulting costs, and enhance ODD responsibilities through the use of customized technology tools which “push” material events communications to those responsible for ongoing ODD.

Institutional investors have a fiduciary obligation to protect the assets entrusted to them by their stakeholders, and overseeing and monitoring material changes specific to their allocations and within the industry is a must. While the level of focus and resources allocated to ongoing ODD is increasing, current processes are generally (1) reactive in nature, (2) dependent upon requesting information or on periodic updates, and (3) are likely not all encompassing, even with respect to specific fund allocations.

Convergence has identified 33 operating complexity factors which it captures and creates, all geared at enabling investors the ability to assess and measure the business risk profile of manager allocations, including the ability to compare and contrast with industry peers.

The Convergence platform captures and creates data on a daily basis covering the entire registered investment advisor universe. Custom data updates are pushed to institutional investors based on their customized requirements, including specific fund allocations and specific data artifacts based on their own assessment of operations-related risk.

ABOUT CONVERGENCE, INC.

Convergence has created an entirely new platform comprising (1) enriched and customized data; (2) research and analytical products; (3) surveillance/ monitoring services; and (4) advisory services, all providing transparency into the infrastructure of the alternative asset management industry.

Please contact George Evans at gevans(at)convergenceinc(dot)com or Joe Dello Russo at jdellorusso(at)convergenceinc(dot)com to learn more about the results of the Convergence ODD study and the Convergence platform and related technology tools available to institutional investors.

APPENDIX

The attached tables are extracts from the final Convergence ODD study report issued to institutional investor survey participants, which will be of interest to those with dedicated ODD staff and those allocating resources to ODD.

Introduction

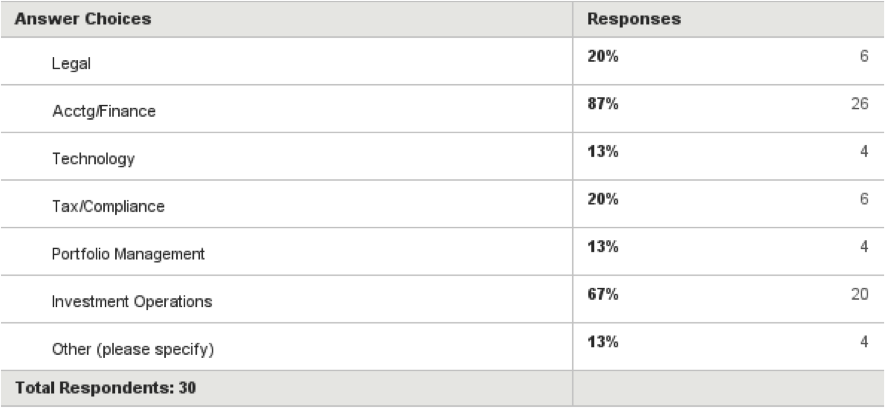

ODD resources are clearly dominated by those with professional backgrounds in (1) accounting and finance, and (2) investment operations. These areas of expertise are consistent with the results below with respect to the allocation of time spent by investors in their ODD activities. However, given the very high focus on “compliance” activities, one could expect a trend of more compliance and legal resources being deployed in conjunction with investor ODD.

TABLE I. ODD Survey Question - What are the Primary Areas of Expertise of your Dedicated ODD Employees (select all that apply)?

Findings - The vast majority of ODD staff at institutional investors is comprised of accounting and finance, and investment operations professionals, as noted below. These skill sets suggest a critical need for focus on internal controls and operations-related processes. In addition, these areas of focus suggest a very “data driven” approach to ODD.

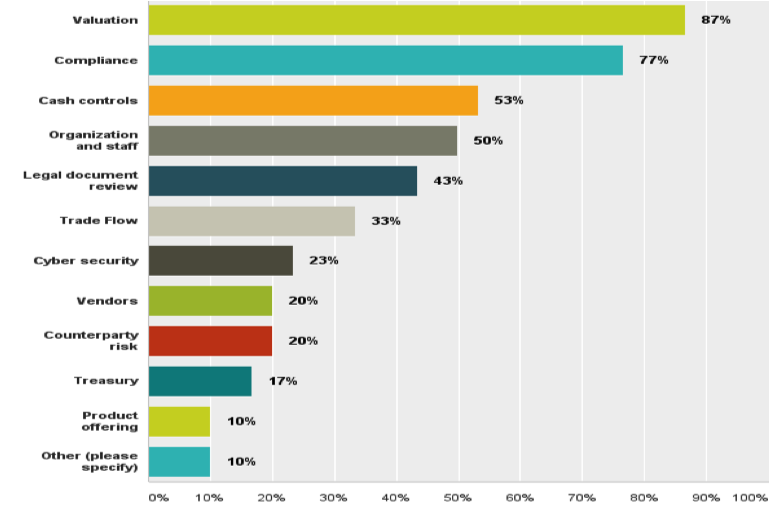

TABLE II. ODD Survey Question - Which Areas of Focus does your Firm Allocate the Highest % of ODD Time (select the top 5 areas)?

Findings – Virtually all institutional investor survey participants cite valuation as a “top 5” area of focus. Beyond valuation, the primary areas of focus revolve around regulatory compliance, the quality of staff and internal processes, and the quality of external service providers critical to the internal control processes of the manager. The Convergence platform enables investors to assess the complete business and operations-related profile of its manager allocations to manager peers.

George Evans, Convergence Inc, http://convergenceinc.com/, +1 2127047100, [email protected]

Share this article