Hamilton Bancorp, Inc. Reports First Quarter Fiscal 2017 Results with Asset Growth of 33 Percent and Revenue Growth of 28 Percent

Towson, MD (PRWEB) August 01, 2016 -- Hamilton Bancorp, Inc. (the “Company”) (NASDAQ: HBK), the parent company of Hamilton Bank (the “Bank”), today announced its operating results for the three month period ending June 30, 2016 with the following highlights:

Quarterly Highlights – Quarter Ending June 30, 2016 vs. March 31, 2016

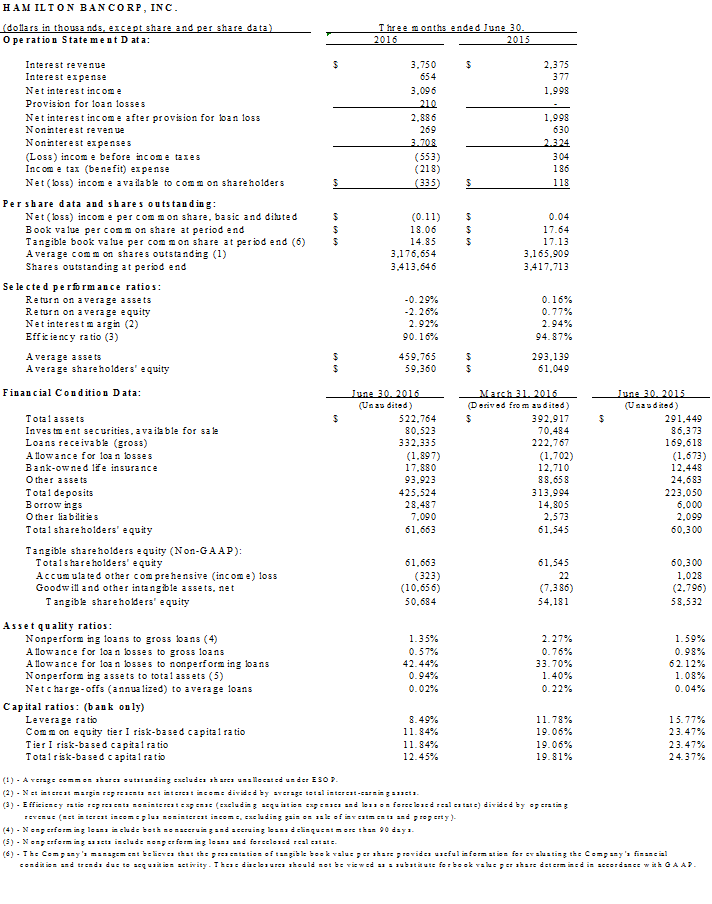

- Total assets grew to $522.8 million, up $129.8 million, or 33 percent, compared to $392.9 million.

- Total gross loans grew to $332.3 million, up $109.6 million, or 49 percent, compared to $222.8 million. Growth in loans was attributable to both the acquisition of Fraternity Community Bancorp, Inc. (“Fraternity”) and organic loan growth. Total deposits grew to $425.5 million, up $111.5 million, or 36 percent, compared to $314 million. This growth included $108.9 million in acquired Fraternity deposits

- Nonperforming loans as a percentage of gross loans declined to 1.35 percent from 2.27 percent.

- The allowance for loan losses as a percentage of nonperforming loans increased to 42.4 percent from 33.7 percent.

- GAAP results reflect a net loss of $355,000 which included $674,000 in acquisition and branch consolidation related expenses, or ($0.11) per common share.

- Non-GAAP net income before tax was $121,000 excluding $674,000 in acquisition and branch consolidation related expenses, or $0.04 per common share.

Quarterly Highlights – Quarter Ending June 30, 2016 vs. June 30, 2015

- Net interest income increased to $3.1 million, up $1.1 million, or 55 percent, from $2.0 million.

- Book value per common share increased to $18.06, up 2 percent, from $17.64.

“We are very pleased with the successful integration of our two acquisitions. The growth experienced in the last year has been significant, not just related to our acquisitions, but through our organic growth in commercial loans and residential construction-permanent loans,” said Robert DeAlmeida, President and CEO. “We continue to remain focused on improving profitability through increased earnings and efficiencies.”

Balance Sheet

Total assets grew $129.8 million, or 33 percent, during the first quarter to $522.8 million at June 30, 2016, compared to $392.9 million at March 31, 2016. The growth was primarily attributable to $155.3 million in assets acquired from Fraternity, net of acquisition accounting adjustments, partially offset by $25.7 million in cash used to fund the transaction.

Cash and cash equivalents at June 30, 2016 remained elevated at $64.8 million compared to $67.4 million at March 31, 2016 as a result of the acquisition and a temporary large deposit related to one customer. It is our expectation that the excess cash, other than the short-term deposit and funds needed for operations, will be used to fund loans and purchase investment securities in the near term.

Total gross loans grew $109.6 million, or 49 percent, to $332.3 million at June 30, 2016 from $222.8 million at March 31, 2016. This growth was in large part due to $108.6 million in merger-acquired loans. In addition, the Company experienced strong commercial and residential construction-permanent loan demand. Total deposits increased $111.5 million, or 36 percent, to $425.5 million at June 30, 2016, from $314.0 million at March 31, 2016. This growth included $108.9 million in merger-acquired deposits. We continue to focus on generating lower cost, core deposits (which includes all deposits other than certificates of deposit) and maintaining maturing certificates of deposits to support continued loan growth.

Credit Quality

Maintaining strong asset quality remains a core management objective. Annualized net charge-offs to average loans decreased to 0.02 percent in the current quarter from 0.22 percent at June 30, 2015. Net charge-offs for the current quarter totaled $15,000, as a result of $31,000 in charge-offs and $16,000 in recoveries. Non-performing loans at the end of the current quarter decreased to $4.5 million from $5.1 million at March 31, 2016 and represented 1.35 percent of gross loans, down from 2.27 percent. This decrease was in large part due to a reduction in loans that are 90 days past due and accruing. Loans 90 days past due and accruing refer to loans that are past maturity and paying, but are in the process of being extended or re-negotiated. Such loans totaled $80,000 at June 30, 2016, down from $708,000 at March 31, 2016.

Income Statement

Net interest income for the quarter ending June 30, 2016 was $3.1 million, up $1.1 million or 55 percent from $2.0 million for the quarter ending June 30, 2015, reflecting the successful completion of our two acquisitions during the last nine months. The increase reflected a $1.4 million, or 58 percent, increase in interest income as average earning assets increased $152.7 million due primarily to loan growth as a result of the acquisitions along with organic loan growth. Partially offsetting the increase in interest income was an increase of $277,000, or 73 percent, in interest expense over that same period. Overall, average interest-bearing liabilities increased $161.7 million, or 77 percent, in large part due to acquisition-related growth. The net interest margin for the three months ending June 30, 2016 was relatively unchanged at 2.92 percent, compared to 2.94 percent at June 30, 2015.

Non-interest revenue for the quarter ending June 30, 2016 was $269,000, or 57 percent, compared to $630,000 for the comparable period last year. The comparable period last year included a $407,000 gain on the sale of the Towson branch property, which closed in early May 2015. Excluding this gain, non-interest revenue increased $46,000, or 21 percent, compared to the comparable period last year. This increase was attributable to increased revenue from bank-owned life insurance, along with higher service fees. There were no gains on the sale of investment securities for the quarter ending June 30, 2016 or 2015.

Non-interest expense in the quarter ended June 30, 2016 was $3.7 million, up $1.4 million, or 60 percent, from the quarter ended June 30, 2015, primarily reflecting the completion of our two acquisitions. The increase also reflected a generally higher level of expenses associated with operating our now larger financial institution, including additional employees and increased costs for federal deposit insurance, data processing, occupancy, equipment, and professional services. Although there are overall added expenses, the acquisitions provided the opportunity to achieve greater economies of scale as reflected in the improvement in the efficiency ratio to 90 percent in the current quarter compared to 95 percent for the quarter ending June 30, 2015. Included in non-interest expense for the current quarter was $674,000 in acquisition and branch consolidation costs. Branch consolidation cost included $437,000 in expense related to the closing of our Cockeysville branch office due to branch overlap. Management continues to focus on reducing operating expenses and achieving higher efficiencies and economies of scale.

GAAP results reflect a net loss of $355,000, which included $674,000 in acquisition and branch consolidation related expenses, or ($0.11) per common share for the current quarter. Non-GAAP net income before tax was $121,000, excluding $674,000 in acquisition and branch consolidation related expenses, or $0.04 per common share for the current quarter compared to $118,000, or $0.04 per common share for the quarter ended June 30, 2015.

Capital

Average shareholders’ equity to average assets remains strong at 13 percent for the quarter ending June 30, 2016. This was down from 20.8 percent a year ago due to the increase in average assets resulting from the two acquisitions which were all cash transactions which had no material impact on equity. All of the Bank’s regulatory capital ratios continued to exceed levels required to be categorized as “well capitalized.” Outstanding shares at June 30, 2016 were 3,413,646, unchanged from March 31, 2016.

Further Information

Management believes that non-GAAP financial measures, including net income pre-acquisition related expenses and tangible book value, provide additional useful information that allows readers to evaluate the ongoing performance of the Company without regard to transactional activities. Non-GAAP financial measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP financial measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP.

Please direct all media inquiries to Kathy Walsh at 410-420-2001 or by email at [email protected]. Please direct investor inquiries for Hamilton Bank to Robert DeAlmeida at 410-823-4510.

###

About Hamilton Bank

Founded in 1915, Hamilton Bank is a community bank with $523 million in assets and $62 million in regulatory capital. The bank has 75 full-time employees and operates seven branch locations across Greater Baltimore, serving the communities of Cockeysville, Pasadena, Rosedale, Towson, Ellicott City and Baltimore in Maryland. Whether online or on the corner, Hamilton Bank is a community bank that cares about its customers. http://www.Hamilton-Bank.com.

Member FDIC and Equal Housing Lender

This press release may contain statements relating to the future results of the Company (including certain projections and business trends) that are considered "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995). Forward-looking statements include statements regarding anticipated future events and can be identified by the fact that they do not relate strictly to historical or current facts. They often include words such as “believe,” “expect,” “anticipate,” “estimate,” and “intend” or future or conditional verbs such as “will,” “would,” “should,” “could,” or “may.” Forward-looking statements, by their nature, are subject to risks and uncertainties. Certain factors that could cause actual results to differ materially from expected results include increased competitive pressures, changes in the interest rate environment, general economic conditions or conditions within the securities markets, legislative and regulatory changes that could adversely affect the business in which Hamilton Bancorp, Inc. and Hamilton Bank are engaged, and other factors that may be described in the Company’s annual report on Form 10-K and quarterly reports on Form 10-Q as filed with the Securities and Exchange Commission. The forward-looking statements are made as of the date of this release, and, except as may be required by applicable law or regulation, the Company assumes no obligation to update the forward-looking statements or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Kathy Walsh, Fallston Group, LLC, +1 4104202001, [email protected]

Share this article