Hamilton Bancorp, Inc. Reports Increased Earnings and Revenue Growth of 16 Percent For the First Quarter of Fiscal 2018

Towson, MD (PRWEB) July 31, 2017 -- Hamilton Bancorp, Inc. (the “Company”) (NASDAQ: HBK), the parent company of Hamilton Bank (the “Bank”), today announced its operating results for the three month period ending June 30, 2017 with the following highlights:

Quarterly Highlights – Quarter Ending June 30, 2017 vs. March 31, 2017

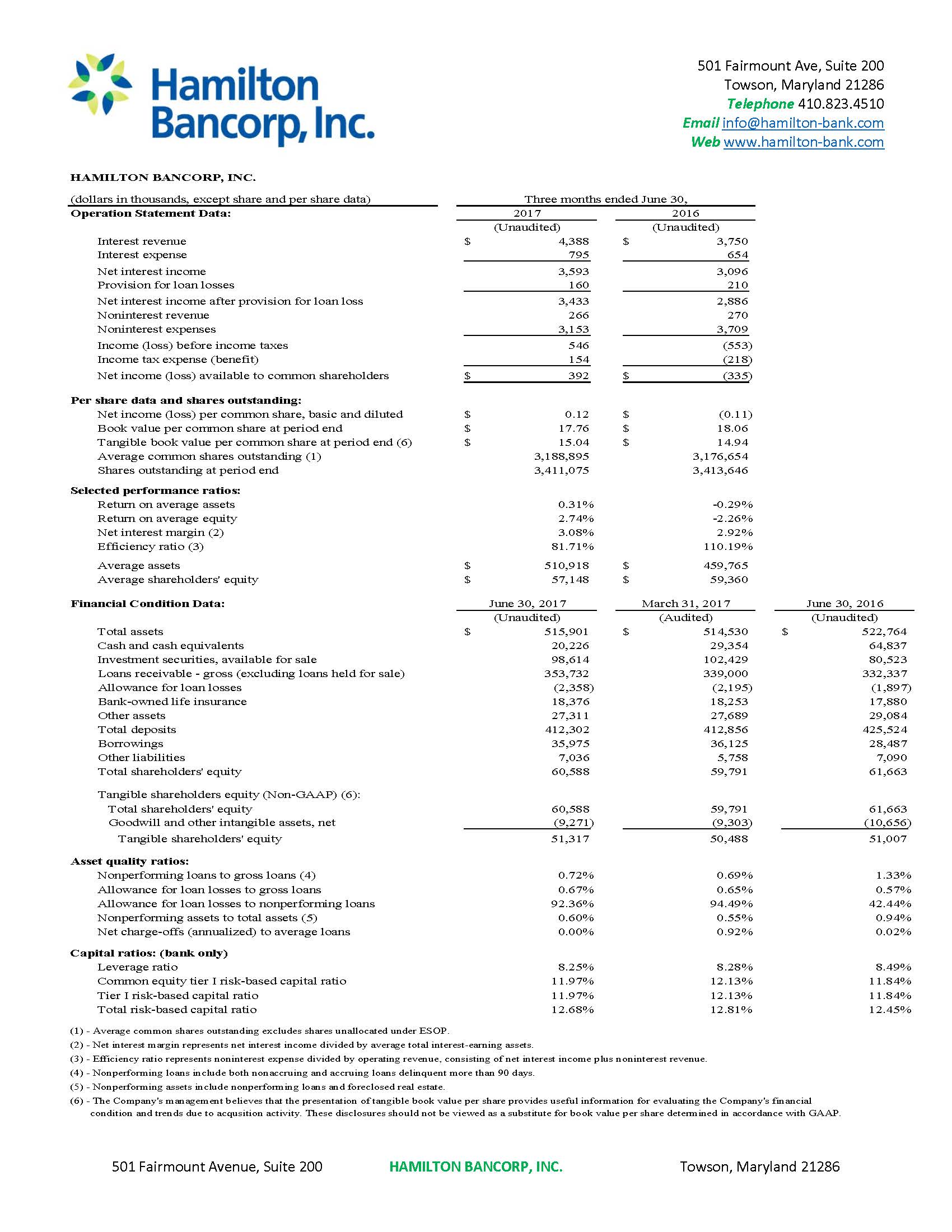

• Net interest margin increased 6 basis points to 3.08 percent during the three months ending June 30, 2017 compared to 3.02 percent for fiscal 2017.

• Total gross loans grew to $353.7 million, up $14.7 million, or 4.3 percent, compared to $339.0 million. Growth in loans was largely attributable to the purchase of a commercial loan portfolio along with organic loan growth. Total deposits remained relatively unchanged, decreasing slightly from $412.9 million to $412.3 million.

• Total assets grew to $515.9 million, or $1.4 million, compared to $514.5 million.

• Core deposits (including all deposits except certificates of deposit) grew $4.5 million to $168.9 million, or 2.7 percent, from $164.4 million. Core deposits represent 41.0 percent of total deposits compared to 33.6 percent a year ago.

• Nonperforming loans as a percentage of gross loans remains low at 0.72 percent compared to 0.69 percent and 1.33 percent at March 31, 2017 and June 30, 2016, respectively.

• The allowance for loan losses as a percentage of nonperforming loans remained relatively unchanged at 92.4 percent compared to 94.5 percent.

Quarterly Highlights – Quarter Ending June 30, 2017 vs. June 30, 2016

• Net income increased $727 thousand to $392 thousand, or $0.12 per common share, compared to net loss of $335 thousand, or loss of $0.11 per common share. Prior year period included $674 thousand in acquisition and branch consolidation related expenses.

• Net interest income increased to $3.6 million, up $497 thousand, or 16 percent, from $3.1 million.

• Net interest margin increased 16 basis points, or 5.5 percent, to 3.08 percent from 2.92 percent.

• Efficiency ratio has decreased by nearly 25 percent from 110.2 percent to 81.7 percent.

• Book value per common share decreased slightly to $17.76, down 2 percent, from $18.06.

“Operating results improved as we continue to see the impact of the change in our balance sheet to lower cost core deposits and the results from our recent acquisitions,” said Robert DeAlmeida, President and CEO. “We have launched our first universal branch model and we will continue to look for ways to innovate and improve efficiencies.”

Balance Sheet

Total assets grew $1.4 million during the first quarter to $515.9 million at June 30, 2017, compared to $514.5 million at March 31, 2017. The growth was primarily attributable to a $14.7 million increase in loans, partially offset by decreases in cash and cash equivalents and the investment portfolio.

Cash and cash equivalents at June 30, 2017 are $20.2 million compared to $29.4 million at March 31, 2017. The decline from March 31, 2017 is a result of cash used to purchase a pool of commercial loans. Proceeds from a declining investment portfolio were also used to fund the loan pool purchase; converting lower interest-earning investments into higher interest-earning loans. Investments declined $3.8 million from $102.4 million at March 31, 2017 to $98.6 million at June 30, 2017. The proceeds from investments during the quarter were a result of normal principal payments associated with the mortgage-backed security portfolio; not from the sale of securities. Excluding funds needed for operations, management intends to utilize any excess cash for future loan growth.

Total gross loans grew $14.7 million, or 4 percent, to $353.7 million at June 30, 2017 from $339.0 million at March 31, 2017. This growth was in large part due to a $15.4 million pool of commercial loans that were purchased at the end of the first quarter of fiscal 2018. Strong commercial real estate and commercial and residential construction loan demand continued to offset run-off from our one-to four-family residential loan portfolio. Growth in commercial business loans resulted in the largest increase in loans increasing $15.8 million, or 73.5 percent, to $37.4 million at June 30, 2017 from $21.5 million at March 31, 2017. As noted earlier, this increase is in large part due to the purchase of a pool of commercial loans. Management is continuing to look at opportunities to diversify our loan portfolio.

Total deposits remained relatively unchanged over the first quarter of fiscal 2018, with $412.3 million at June 30, 2017 compared to $412.9 million at March 31, 2017. The Company continues to focus on generating lower cost, core deposits (which includes all deposits other than certificates of deposit) and maintaining maturing certificates of deposit to support continued loan growth. Core deposits at June 30, 2017 were $168.9 million compared to $164.4 million at March 31, 2017, an increase of $4.5 million, or 2.7 percent for the quarter. On a year-over-year basis, core deposits have increased $26.9 million and represent 41.0 percent of total deposits at June 30, 2017 compared to 33.6 percent of deposits at June 30, 2016.

Credit Quality

Asset quality is strong and remains a core management objective. Non-performing loans at June 30, 2017 increased roughly $230 thousand in the first quarter of fiscal 2018 to $2.5 million at June 30, 2017 from $2.2 million at March 31, 2017. Non-performing loans at June 30, 2017 included $331 thousand in loans that were 90 days past due and accruing. As a result, the percentage of nonperforming loans to gross loans increased slightly from 0.69 percent at March 31, 2017 to 0.72 percent at June 30, 2017, but remains relatively low. The allowance for loan losses as a percentage of nonperforming loans at June 30, 2017 is 92.4 percent compared to 94.5 percent at March 31, 2017 and also remains strong. Annualized net charge-offs to average loans was zero percent for the current quarter ending June 30, 2017, compared to 0.92 percent for fiscal 2017 and 0.02 percent for the comparable quarter ending June 30, 2016. The Company experienced net recoveries totaling $3 thousand over the first quarter comprised of $4 thousand in charge-offs and $7 thousand in recoveries.

Income Statement

Net income for the quarter ending June 30, 2017 was $392 thousand, or $0.12 per common share, compared to a loss of $335 thousand, or a loss of $0.11 per common share for the quarter ending June 30, 2016; an increase of $727 thousand quarter-over quarter. The increase in net income was driven by an increase in net interest income associated with growth in loans, improvement in net interest margin due to the growth in core deposits and a reduction in noninterest expense resulting from acquisition and branch related expenses that were incurred in the prior period.

Net interest income for the quarter ending June 30, 2017 was $3.6 million, up $497 thousand or 16 percent from $3.1 million for the quarter ending June 30, 2016, reflecting the successful completion of the Fraternity Community Bancorp, Inc. (“Fraternity”) acquisition in May 2016 and the continued growth in our loan portfolio from loan purchases and organic growth. The increase reflected a $638 thousand, or 17 percent, increase in interest income as average earning assets increased $42.9 million from investments and loan growth that stemmed from acquisition and organic growth and the purchase of specific loan portfolios. Partially offsetting the increase in interest income was an increase of $141 thousand, or 22 percent, in interest expense over that same period. Overall, average interest-bearing liabilities increased $44.8 million, or 12 percent, in large part due to acquisition-related growth in deposits and increased borrowings to fund loan purchases. The net interest margin for the three months ending June 30, 2017 increased 16 basis points to 3.08 percent, compared to 2.92 percent for the three months ending June 30, 2016.

Non-interest revenue for the quarter ending June 30, 2017 was $266 thousand compared to $270 thousand for the comparable period last year. Non-interest revenue was flat because no loans were sold in the first quarter of fiscal 2018 as the Company held in portfolio the majority of our residential loan originations to partially offset the increased run-off associated with this loan type. Service charges increased $24 thousand, or 25 percent, to $119 thousand as a result of the increase in transactional accounts. There were no gains on the sale of investment securities for the quarter ending June 30, 2017 or 2016.

Non-interest expense for the quarter ended June 30, 2017 was $3.2 million, down $556 thousand, or 15 percent, from the quarter ended June 30, 2016. The decline is primarily the result of $626 thousand in costs associated with the completion of our most recent acquisition in the prior year quarter. While overall operating expenses are higher as a result of operating as a larger financial institution, greater economies of scale have been achieved as reflected in the improvement in our efficiency ratio from 110.2 percent for the three months ending June 30, 2016 to 81.7 percent for the three months ending June 30, 2017. As noted earlier, some of these efficiencies are derived from the elimination of costs associated with the most recent acquisition.

From an operational standpoint, salary and benefit expenses for the first quarter of fiscal 2018 increased $121 thousand compared to the same quarter a year ago as a result of strategic new hires focused on branch efficiency and new products. The Company also recognized one-time increases in occupancy expense due to our re-location of the Ellicott City branch that occurred in July 2017 and legal costs associated with certain loan purchases and other administrative matters. These increases were offset by decreases in other expenses largely composed of data processing and deposit insurance premiums. Management remains committed to reducing operational expenses and achieving higher efficiencies.

Capital

Average shareholders’ equity to average assets was 11.2 percent for the quarter ending June 30, 2017. This is down from 12.9 percent a year ago due to the increase in average assets resulting from the most recent acquisition, which was an all cash transaction and had no material impact on equity, and growth from both organic loans and loan purchases. All of the Bank’s regulatory capital ratios continue to exceed levels required to be categorized as “well capitalized.” Outstanding shares at June 30, 2017 were 3,411,075, unchanged from March 31, 2017.

Further Information

Management believes that non-GAAP financial measures, including tangible book value, provide additional useful information that allows readers to evaluate the ongoing performance of the Company without regard to transactional activities. Non-GAAP financial measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP financial measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP.

Please direct all media inquiries to Lauren Lawder at 410-616-1996 or by email at [email protected]. Please direct investor inquiries for Hamilton Bank to Robert DeAlmeida at 410-823-4510.

###

About Hamilton Bank

Founded in 1915, Hamilton Bank is a community bank with $516 million in assets and $61 million in regulatory capital. The bank has 75 full-time employees and operates seven branch locations across Greater Baltimore, serving the communities of Cockeysville, Pasadena, Rosedale, Towson, Ellicott City and Baltimore in Maryland. Whether online or on the corner, Hamilton Bank is a community bank that cares about its customers. http://www.Hamilton-Bank.com.

Member FDIC and Equal Housing Lender

This press release may contain statements relating to the future results of the Company (including certain projections and business trends) that are considered "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995). Forward-looking statements include statements regarding anticipated future events and can be identified by the fact that they do not relate strictly to historical or current facts. They often include words such as “believe,” “expect,” “anticipate,” “estimate,” and “intend” or future or conditional verbs such as “will,” “would,” “should,” “could,” or “may.” Forward-looking statements, by their nature, are subject to risks and uncertainties. Certain factors that could cause actual results to differ materially from expected results include increased competitive pressures, changes in the interest rate environment, general economic conditions or conditions within the securities markets, legislative and regulatory changes that could adversely affect the business in which Hamilton Bancorp, Inc. and Hamilton Bank are engaged, and other factors that may be described in the Company’s annual report on Form 10-K and quarterly reports on Form 10-Q as filed with the Securities and Exchange Commission. The forward-looking statements are made as of the date of this release, and, except as may be required by applicable law or regulation, the Company assumes no obligation to update the forward-looking statements or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Andrea Lynn, Fallston Group, LLC, http://www.fallstongroup.com/, +1 (410) 420-2001, [email protected]

Share this article