AUSTIN, Texas, Dec. 11, 2018 /PRNewswire-PRWeb/ -- DSCC released its latest Quarterly Display Capex and Equipment Service suite of products which includes:

- Display equipment spending forecasts by equipment supplier, equipment segment, display frontplane technology, display backplane technology, glass size, flexible vs. rigid, manufacturer, country, etc. This deliverable includes fab by fab equipment spending by equipment type and equipment supplier revealing design wins and market share for nearly 40 different types of equipment.

- Display capacity forecasts by panel supplier, country, frontplane technology, backplane technology, glass size, flexible vs. rigid, etc.

- Display equipment supplier financials for 21 equipment companies and panel supplier capex and financial data for 11 different panel suppliers.

One of the highlights of the latest report was that Q3'18 was a record quarter for display equipment spending and capex with five G6 OLED lines installed as well as a 10.5G line. As shown below:

- Total display capex was $11.1B, up 32% Q/Q and 18% Y/Y. Publicly traded display companies accounted for 52% of capex with private companies at 48%.

- Display equipment spending also reached a new high in Q3'18 up 71% Q/Q and 13% Y/Y to a record $7.3B.

- Display equipment revenues for 21 publicly traded equipment suppliers also reached a new high at $3.8B led by Canon and Applied Materials.

The top 5 equipment suppliers in Q3'18 and their respective market shares were:

- Canon – 13.1%

- Applied Materials – 9.6%

- Tokyo Electron – 4.6%

- Nikon – 4.3%

- SFA Engineering – 4.1%

The next 5 were ULVAC, V-Technology, AP Systems, SCREEN Holdings and Orbotech.

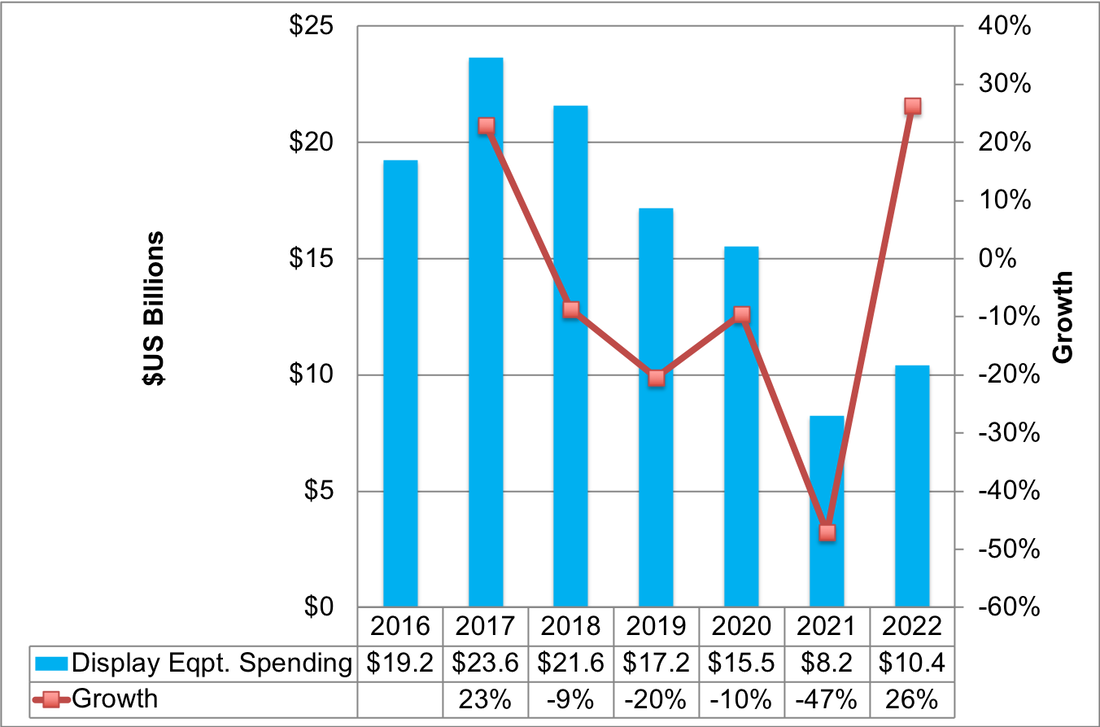

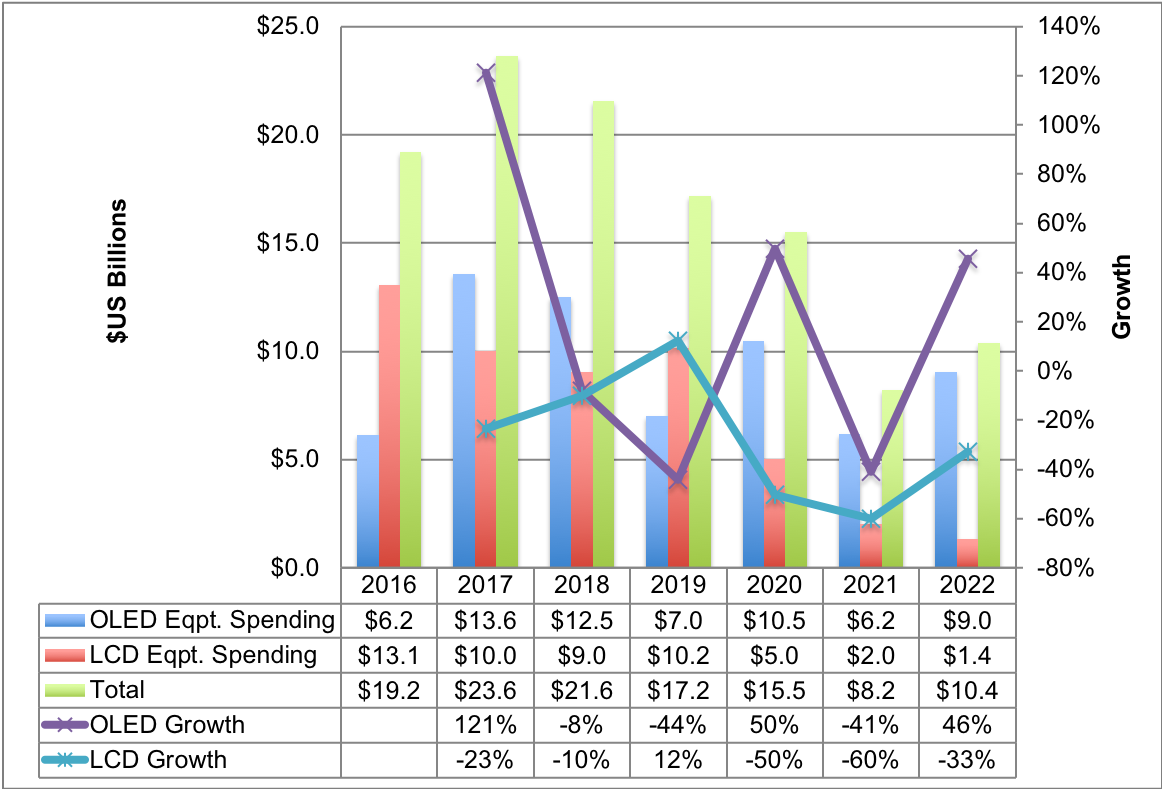

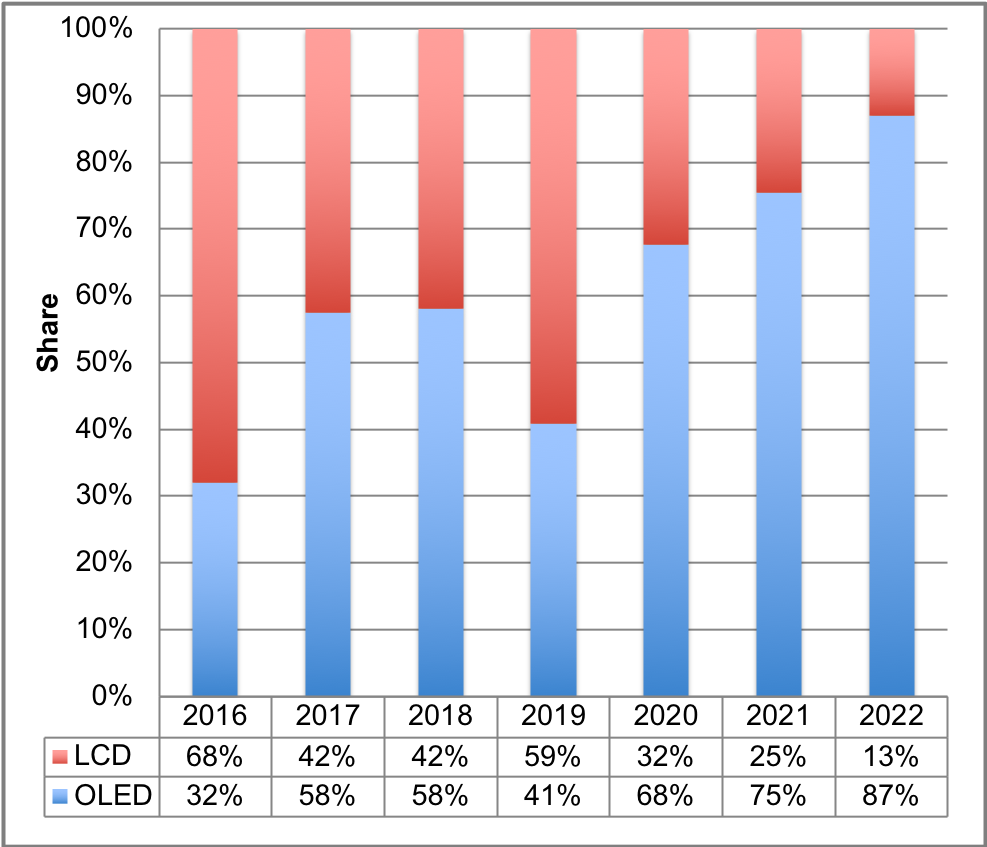

Display equipment spending through 2022 is shown in the attaced table and is expected to fall 9% in 2018 despite the record Q3'18 to $21.6B, the second highest total to date. In 2018, OLEDs are expected to maintain a 58% share of spending on an 8% decline to $12.5B. LCD spending is expected to fall 10% to $9B.

In 2019, LCD spending is expected to rise 12% as 10.5G fab spending soars from 20% of total display equipment spending in 2018 to 43% in 2019. The LCD share of equipment spending is expected to rise to 59% of total spending as OLED equipment spending drops 44% to $7B as mobile OLED spending slows.

In 2020, OLEDs are expected to rebound, rising 50% to $10.5B with its share of equipment spending rising to 68% on gains in both mobile and TV OLED equipment spending. On the other hand, LCD equipment spending is expected to slow, falling 50% as 10.5G LCD equipment spending declines.

In 2021, DSCC expects both OLED and LCD equipment spending to decline. In 2022, OLEDs are expected to rebound on gains in both mobile and TV, while LCD spending continues to slide on saturation and slower growth concerns. The OLED share of display equipment spending is expected to reach 75% in 2021 and 87% in 2022 as shown in the attached figure.

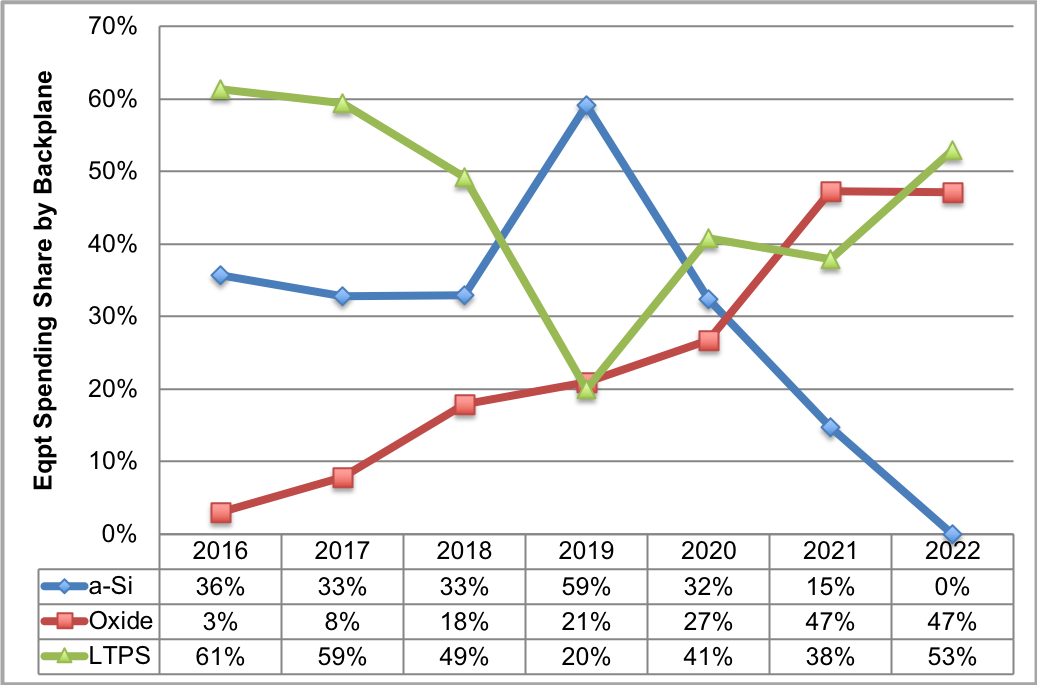

Another interesting variable to look at is display equipment spending by backplane technology. As shown below, the metal oxide spending share is growing rapidly due to significant growth in OLED TV fab equipment spending as well as smaller expenditures in mobile LCDs and OLEDs and 8K LCDs. The oxide share of fab spending is expected to rise from 3% of spending in 2016 to 47% of spending in 2021 and 2022. The LTPS spending share is expected to fall from around a 60% share in 2016 and 2017 to just 20% in 2019 as mobile spending cools on a significant oversupply. However, it will eventually rebound to over a 50% share in 2022 as mobile spending heats up again as high resolution OLEDs increase their penetration into applications beyond smartphones.

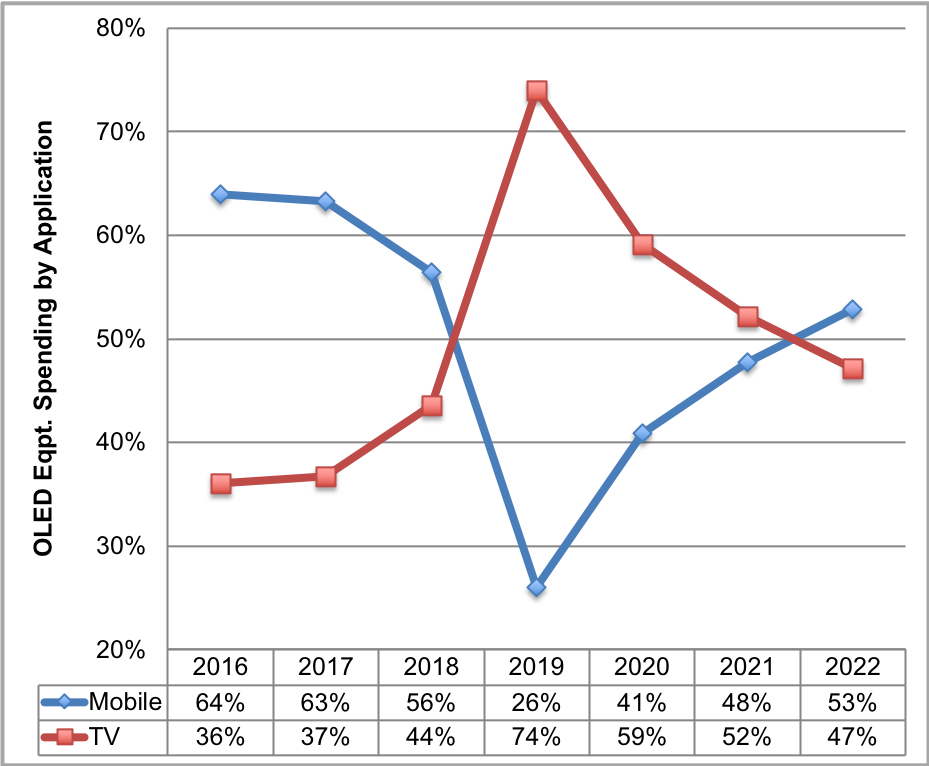

Speaking of applications, display equipment spending is shown by application in the attached tables. As indicated, TV spending is expected to drive the market accounting for a majority of display equipment spending from 2019 – 2021 after accounting for a minority of equipment spending from 2016-2018. TV spending will benefit from significant expenditures on expensive 10.5G LCD fabs optimized for lower cost production of larger LCD TV sizes as well as increased spending on different flavors of OLED TV fabs which are even more expensive due to higher process complexity.

The elevated equipment spending levels show that display manufacturers continue to bring larger and more advanced displays to the market enabling better visual experiences for the consumer. For more information on DSCC's Quarterly Display Capex and Equipment Service including its extensive capacity database and forecasts, please contact [email protected].

About Display Supply Chain Consultants (DSCC)

Display Supply Chain Consultants (DSCC) was formed by experienced display market analysts from throughout the display supply chain and delivers valuable insights through consulting, syndicated reports and events. The company has offices in Korea, China, Japan and the US, is on the web at http://www.displaysupplychain.com and can be reached in the US at [email protected] and (512) 577-3672.

SOURCE Display Supply Chain Consultants

Share this article