Think Zinc Markets: An Enigma Wrapped in Potential

Vancouver, BC (PRWEB) January 29, 2014 -- Arguably not the sexiest of metals, zinc is essential to a myriad of industrial uses and a critical component in the growing global demand for steel production. With almost 3.4 billion pounds of global zinc production set to disappear through 2015, new resources coming online should demand investor attention.

The enigma results from stalled zinc prices in the face of ongoing mine closings, either actual or planned over the next few years with an attendant decline in supply. That supply/demand/price contradiction could well be about to change.

Zazu Metals (ZAZ.TO), a relative unknown in the investor world, appears set to be a large part of the supply solution. As the operator of the advanced stage zinc, lead and silver Lik property in NW Alaska, the Company boasts 50% partner Teck (operator of the nearby world-class Red Dog mine) access to purpose built State-owned road and port, no debt and $2 million in the treasury. Zazu’s release of a 2014 PEA (Preliminary Economic Assessment) is imminent, which will give hard numbers and likely further confirm the compelling potential –large tonnage, high grade--of this project.

High zinc production costs in China have pushed imports to a 12-month high with Asia sucking up the largest percentage of global zinc demand. Steel production is forecast to increase 3.3% globally to 1.52 billion tonnes in 2014.

Further, while LME(London Metals Exchange) inventories were at a record high at 1.2 million tonnes last summer that number continues to decline and currently sits at roughly 800 million tonnes creating a supply gap that ultimately needs to be filled.

“There are no obvious impediments ahead to put Lik into production,” stated Matthew Ford, President of Zazu. “ The project has the tonnage, grade and metallurgy to be a mine. It has access to nearby hauling and shipping infrastructure and is in a mining friendly jurisdiction. It has local and governmental support and is well prepared to enter mine permitting."

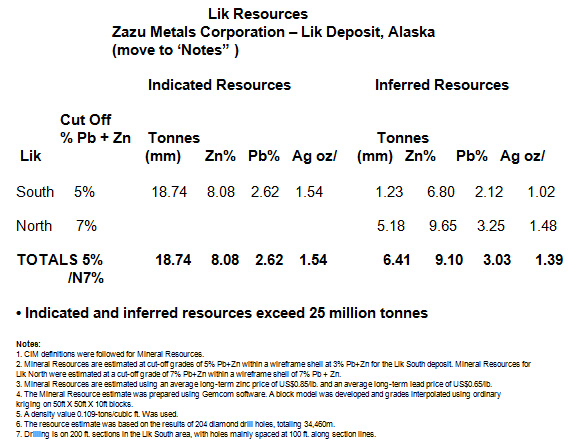

Here are the Lik property details:

Deposit Size, Grade, Location and Description:

Click here for Lik Indicated and Inferred Resources

Lik South is around 1.1 km on strike and 600m wide. The Company expects this portion to be an open pit configuration.

Lik North has over 5mm tonnes of inferred resource grading at 8.9% zinc. The claim extends several kilometers north, allowing for significant expansion.

The anomaly here is the low price in the face of looming and documented supply shortages.

Higher prices and tighter/lower inventories bode well for juniors such as Zazu. Those eventualities would likely cause more production to come on stream, stabilize the market and address the demand issues.

The reason Zazu should be of interest to investors is, as Matt Ford states, “The property checks all the boxes for investors.”

Taking away the infrastructure headaches allows the Company to focus on moving toward production. The property itself has close to surface large tonnage, the infrastructure is in place and available—with the potential for state-funded expansion—and the area is in a mining friendly state and community.

One of the main issues with any mine is the cost of infrastructure—getting material to transportation/market. That ceases to be a concern for Zazu and ultimately shareholders. The road necessary to connect with the road from port to Red Dog would likely be funded by AIDEA (Alaska Industrial Development and Export Authority), a public corporation of the State. Any monies spent by a third party such as AIDEA, would count against the $40 million Zazu has the right to spend to acquire 60% 0f Teck’s 50% of Lik, taking Zazu’s interest to 80%.

That road would also open up Teck’s Su deposit, which lies between Lik and Red Dog: Another tenet that speaks to the possible amalgamation/acquisition of Lik by Teck. Time will tell.

The established potential of the Lik property, the relationship and attendant benefits to a partnership with the main player in the global zinc market, the added bonus of lead and silver revenues and the strong support of the state and local governments pretty much counter those seemingly contrary offsets.

The PEA is pending and will be out soon. That document will give investors and the market the numbers they need: And, of course, Zazu itself.

Legal Disclaimer/Disclosure:

A fee has been paid for the production and distribution of this Report. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. No information in this article should be construed as individualized investment advice. A licensed financial advisor should be consulted prior to making any investment decision. Financial Press makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of the author’s only and are subject to change without notice. Financial Press assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this article and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this article.

Also, please note that republishing of this article in its entirety is permitted as long as attribution and a back link to FinancialPress.com are provided. Thank you.

Matthew Ford, Zazu Metals Corporation, http://www.zazumetals.com/, +1 210-858-7512, [email protected]

Share this article