New Research from Wilmington Trust Finds Nearly 60 Percent of Business Owners Lack a Transition Plan

Wilmington, Del. (PRWEB) September 14, 2017 -- A new survey from Wilmington Trust and a team of academic advisors found that 58 percent of owners of privately-held businesses lack a transition plan despite financial risks of not planning. The research, titled “The Power of Planning,” surveyed more than 200 owners of privately-held companies about their plans and goals for transitioning their business.

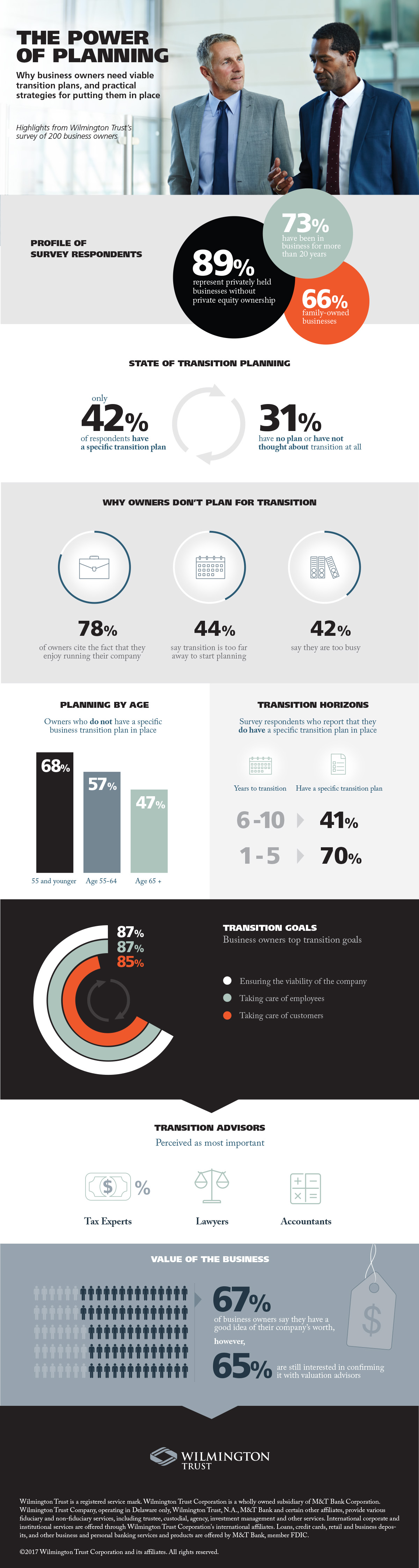

According to the research, the top reason for business owners delaying transition planning was their passion for the day-to-day logistics involved in running their companies. Seventy-eight percent of business owners who did not have a transition plan said they enjoy managing their company too much to start thinking about a future transition. Further, 42 percent responded they were too busy to start planning, while 44 percent felt that a transition was too far in the future to establish a plan.

“Business owners love what they do, so it can be difficult for them to imagine a day when they need to give it up,” said Matt Panarese, president of Wilmington Trust’s Mid-Atlantic region and leader of the firm’s National Business Owner Practice Group. “The reality is that planning effectively and running a business are not mutually exclusive. Owners don’t need to walk away from the business they’ve spent their lives building to start thinking long-term. In fact, early planning can provide more flexibility and allow owners to continue to work in whatever capacity they choose—before and after a transition.

“What business owners need to realize is the sooner they start planning, the better their odds of achieving their goals—both financial and personal. While some owners may be closer to a transition point than others, it’s not too late to create a meaningful plan.”

Surprisingly, 47 percent of respondents age 65 or older still do not have a transition plan in place. Yet 67 percent of all respondents said getting older is the top reason for creating a plan, followed by providing security for their family (55%). Rounding out the top five reasons to have a plan are:

• Meeting the valuation goal – 36%

• Reducing tax – 35%

• Receiving an offer from a potential buyer – 22%

When asked to describe the status of their future plans, business owners without an existing transition plan (58%) said they:

• Have broad outlines, but nothing specific – 27%

• Have considered, but haven’t start planning – 20%

• Have not thought about transition at all – 11%

Conversely, business owners who’ve already established a transition plan (42%) said they:

• Have a specific plan and have begun executing – 21%

• Have a specific plan, but have not begun executing – 21%

“There are many good reasons for business owners to start long-term planning,” said Stuart Smith, managing director of the M&T Investment Banking Group, which, along with Wilmington Trust, is part of the M&T Bank family of companies. “Advance planning enables owners to continue to run the business they’ve built, while addressing financial security for themselves and their families. It can also help them obtain a better result once they decide to transition.

“Business owners have a singular focus on ensuring their companies continue to thrive, so allocating time to build a transition plan can be perceived as a distraction from important work. The truth is planning is important work.”

The survey results show that business owners have both a professional and emotional connection to their companies, and a sense of personal responsibility that extends beyond the company to employees and customers. The two most important transition goals cited by survey respondents were “ensuring the company remains viable in the long-run” and “taking care of employees,” both cited by 87 percent of respondents.

Coming in a close second was “ensure your customers are taken care of” at 85 percent. In third place, at 83 percent, was “financial security for you and family.” Concern for family, employees, and the company continue to round out transition goals, with respondents citing the following motivators:

• Ensure your company retains value – 78%

• Maintain family harmony – 58%

• Keep the business within the family – 39%

• Pass control to employees – 28%

“Ownership transition represents the culmination of one’s business life—a significant and demanding endeavor requiring blood, sweat, and tears over the years,” said Thomas Schwarz, founder and senior counsel at Black Forest Business Solutions. “Without careful consideration of the full range of personal and professional goals, as well as the complexity of the process, it is likely that some of the owner’s goals will be left unmet.

“To avoid regrets and ensure post-transition wealth is directed toward meeting their important goals, owners need to embrace long-term planning and work with a highly capable team of transition experts that see and deal with these issues every day.”

The survey also explored perceptions of business owners about selecting transition advisors. More than 80 percent of owners listed tax expert (84%), lawyer (83%) and accountant (83%) as the top three most important advisors. Other top advisors include:

• Legal Trust Expert – 65%

• Banker – 45%

• Investment Advisor – 40%

• Family Business Consultants – 14%

• Executive Coach – 14%

“Business owners should avoid relying too heavily on a few advisors,” said Panarese. “Business transitions are a team sport. De-emphasizing other experts can create barriers to executing a successful transition. Today’s business environment is more complex than ever, so owners need advice from a broad group of experts, including wealth advisors and investment bankers, who can play a critical role in drawing resources together to successfully navigate a transition.”

Within the circle of advisors, business valuation experts play a critical role for owners. While two-thirds of survey respondents say they have a very good sense of their company’s worth, the same percentage (67%) want to speak with valuation experts.

Valuation is clearly a top concern for business owners, but they have competing goals of taking care of employees and customers. They also care about the intertwined legacy for themselves and their companies.

“Many privately-held companies we work with bear the name of the owner on the building, letterhead, and even products, so business transition becomes a very personal experience,” said Smith. “There are times when we recommend a seller consider a buyer who is not necessarily offering the most money, but shares the same values. Often a buyer who can help the business owner satisfy multiple goals related to family, employees and clients is better choice than the one with the highest financial offer.”

ABOUT THE SURVEY

Researchers surveyed more than 200 business owners in North America, of which:

• 89% owned privately-held companies without private equity investors

• 66% had a family-owned business

• 73% had been in business for more than 20 years

• 81% had annual sales revenue over $10 million

• 52% had more than 50 full-time employees

The full survey, including recommendations for building a robust transition plan, is available online at http://www.WilmingtonTrust.com/BusinessOwners.

ABOUT THE ACADEMIC ADVISORS

Matt Allen, PhD, is associate professor at Babson College, and faculty director for the college’s Institute for Family Entrepreneurship.

Francesco Barbera, PhD, is senior lecturer and co-director of the Family Business Education and Research Group at the University of Adelaide.

Thomas Schwarz, PhD, is founder and senior counsel at Black Forest Business Solutions, and former dean of Stetson University’s School of Business Administration. He was also a visiting scholar at Babson College.

ABOUT WILMINGTON TRUST

Wilmington Trust’s Wealth Advisory offers a wide array of personal trust, financial planning, fiduciary, asset management, *private banking, and family office services designed to help high-net-worth individuals and families grow, preserve, and transfer wealth. Wilmington Trust focuses on serving families with whom it can build long-term relationships, many of which span multiple generations.

Wilmington Trust’s National Business Owner Practice Group is comprised of wealth management and commercial banking leaders, who provide strategic direction for this key segment of the bank. The practice group provides thought leadership, research, analytics, and support to teams across the organization that engage with business owners.

Wilmington Trust also provides Corporate and Institutional Services for clients around the world.

Wilmington Trust has clients in all 50 states and in more than 90 countries, with offices throughout the United States and internationally in London, Dublin, and Frankfurt. For more information, visit http://www.WilmingtonTrust.com.

MEDIA CONTACT: Kent Wissinger, Wilmington Trust PR Manager (302)651-8758

Wilmington Trust is a registered service mark. Wilmington Trust Corporation is a wholly owned subsidiary of M&T Bank Corporation. Wilmington Trust Company, operating in Delaware only, Wilmington Trust, N.A., M&T Bank and certain other affiliates, provide various fiduciary and non-fiduciary services, including trustee, custodial, agency, investment management and other services. International corporate and institutional services are offered through Wilmington Trust Corporation's international affiliates. Loans, credit cards, retail and business deposits, and other business and personal banking services and products are offered by M&T Bank, member FDIC.

*Private Banking is the marketing name for an offering of M&T deposit and loan products and services.

Kent Wissinger, Wilmington Trust, http://www.wilmingtontrust.com, +1 (302) 651-8758, [email protected]

Share this article