For the last few years, the real estate market has been scorching-hot, especially in cities with fast-growing populations. Cracks have begun to appear in many markets specifically the Washington DC, Maryland, & Northern Virginia markets.

BETHESDA, Md., June 2, 2022 /PRNewswire-PRWeb/ -- For the last few years, the real estate market has been scorching-hot, especially in cities with fast-growing populations. Cracks have begun to appear in many markets around the country. This boom was driven by multiple factors, such as the pandemic, Wall Street hedge funds, and boomers wanting a second or third home. But, one unfortunate side effect of the real estate market has been inflation. So, to cool the market, the Fed has begun to raise interest rates.

As of May 2022, it seems the Fed's efforts are starting to battle inflation. We're seeing a shift within the industry and a cooling-off period that could last years, depending on how it all shakes out. Home sales have already begun to drop, fewer buyers are seeking mortgages because they simply can no longer afford to purchase. This shift has happened in record time, which is even more concerning given how most statistics are between 30 and 90 days old. It's imperative to stay on top of trends so we can anticipate changes as they happen, not after the fact.

So, what's driving this shift? It's a double whammy of high prices, higher interest Higher mortgage rates. The Fed has steadily increased these rates to their highest levels since 2011 after the Great Recession. As of May 2022, a 30-year fixed mortgage (the most common option for most home buyers) is over 5.25 percent. Back in January, it was only at 3.22 percent. Such a substantial jump has vast ramifications for both buyers and sellers. This is also the fastest mortgage rate increase since 1994.

What High Rates Mean for Buyers

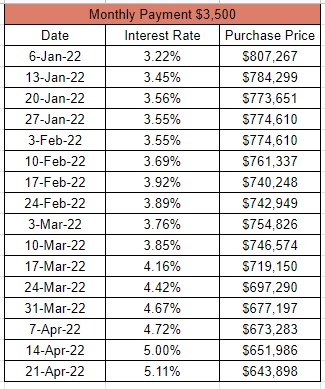

A couple of percentage points doesn't look like much on paper, but each one represents a significant loss in buying power. As a rule, for every one percent increase, a buyer loses about 10 percent of their buying power. The reason is that more of their money goes toward interest and not the principal balance. So, a higher rate can price many people out of various homes because they just can't afford to pay the higher interest. To illustrate this effect further, check out this table, which highlights how much a $3,500 monthly payment can buy based on the current interest rate.

How High Rates Affect Sellers

When the market is red-hot, sellers can often accept cash offers or experience bidding wars for their property. After a while, every seller starts seeing dollar signs and coming up with unrealistic expectations of their listing price. Typically, there are two ways that this manifests. First, a seller tells themselves they only need X amount. Secondly, they think, "the house down the street sold for X, and my house is nicer, so I should be able to sell it for Y."

Let's break down both of these mistakes from an objective standpoint.

I Just Need $X

From a seller's perspective, the listing price is often based on their personal needs. They bought the home for a certain amount, and they want (or need) to make X profit on the sale. Unfortunately, homebuying isn't just about the seller - there are many other people and entities involved.

For example, when the seller bought their house, how much did they consider that seller's needs? Similarly, the appraiser and the mortgage lender don't care about what the seller wants - they're only interested in how much the property is worth, full stop. When it comes to appraising a property, most factors are out of the seller's control, including elements like mortgage rates.

The House Down the Street Sold for X, and My House is Nicer

The real estate market can shift rapidly and on a dime. As you noticed from the illustration above, interest rates can change in weeks or days. So, just because a property sold recently doesn't mean the situation is the same for the seller's home. Also, many sellers don't realize how much time it takes to close a deal. Even if that house sold a few days ago, the contract is likely more than a month old.

In many cases, sellers get into denial and look for agents who will show them data they like, not necessarily recent or accurate information. As a real estate agent, it's my job to provide the most accurate data possible, regardless of how it affects the seller's mood. Emotions cannot dictate the home buying or selling process, especially because so many people are involved.

We've seen time and again when sellers let their history or financial needs inflate the value of their property. In an upward market, this tactic isn't so bad because the market will rise to meet the inflated price. But, in a downward market, like we're seeing now in DMV and elsewhere, overvaluing property can lead to significant problems. In most cases, the seller winds up settling for much less than they could have sold for if they priced their home correctly the first time.

The most effective and safest pricing strategy in a slowing market is to price about 3-5% below the last sold comparable (no more than 14 days old) as long as the price is below the current compatible by at least 2%. This encourages motivated buyers to bid up the final number. But, an overpriced home will sit on the market too long and seem like a bad investment.

Based on the current trends, we can expect home prices to fall between five and 10 percent over the next couple of years. Also, that's up to 10 percent less than the current market value, not an overinflated "I want X" price. According to Redfin, home prices have dropped by as much as 14 percent in April alone.

Breaking Down the Driving Factors

Buying or selling a home should be a relatively objective process, so it helps to understand the factors that determine shifting trends. Here's a breakdown of what's driving this current downturn:

- The Federal Reserve - This entity exists solely to protect the US dollar and ensure it remains the world currency. So, the Fed adjusts interest rates based on national interests, not how it will affect homeowners.

- The Economy - One primary reason the Fed raised rates was to slow inflation. High inflation can lead to unemployment and poverty, which are dangerous if left unchecked. Unfortunately, the Fed's actions may inadvertently lead to higher unemployment and worse inflation if there is no course correction later on.

The Bottom Line

If you're trying to buy or sell a home right now, the shifting market may change your plans. This shift will likely play out over the next three to five years, so your actions can make a huge difference over the long term. Right now, home prices will likely stay flat or go down while the dollar's value weakens from inflation.

Media Contact

Marc Cormier, Berkshire Hathaway Pen Fed Realty, 1 301 660-6272 Ext: 711, [email protected]

SOURCE Berkshire Hathaway Pen Fed Realty

Share this article