Cloud Services Market Will Accelerate to 24% Growth Rate Through 2024 as Hyperscalers and Non-Hyperscalers Battle for Market Share--Everest Group

Hyperscalers will seize more of enterprise IT spend, but other infrastructure vendors will continue to be relevant

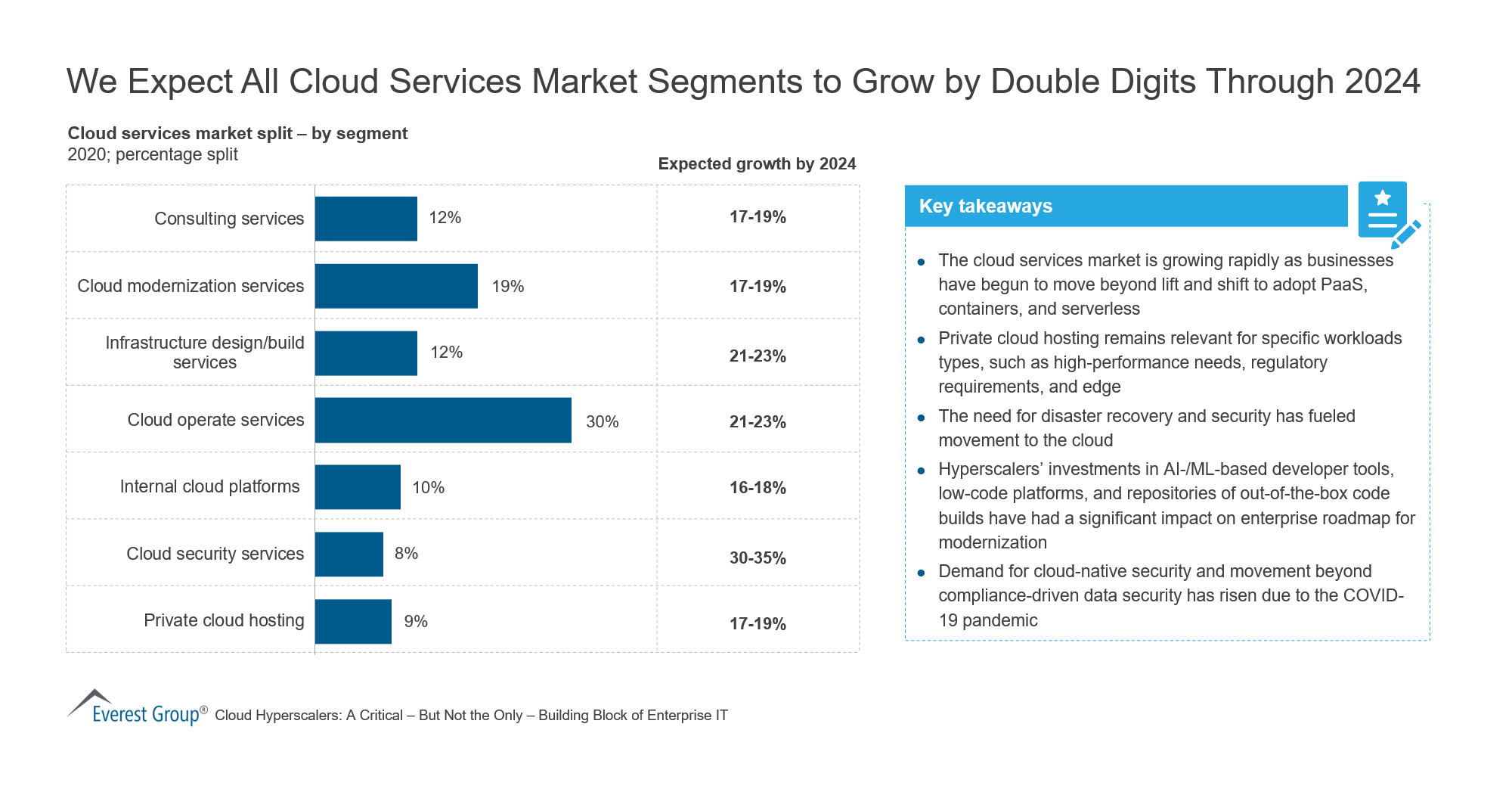

DALLAS, July 19, 2021 /PRNewswire-PRWeb/ -- Hyperscale public cloud providers have experienced growth rates exceeding 30% for the past few years, and their appetite for enterprise IT spend remains insatiable. Everest Group predicts hyperscalers—namely Amazon Web Services (AWS), Google Cloud, and Microsoft Azure—will seize more of enterprise IT spend as the cloud services market accelerates to 24% compound annual growth rate through 2024. However, enterprises will continue to demand a diverse vendor portfolio to avoid lock-in, address data security and governance concerns, build innovative consumption and commercial models, and take advantage of vendors' unique strengths.

More than 90% of enterprises already leverage one or more public clouds in their enterprise environment. COVID-19 has further accelerated enterprise migration to the public cloud, with most enterprises reaping business continuity benefits during the pandemic. Hyperscalers plan to capitalize on this growth and dominate the enterprise IT spend by expanding their offerings beyond infrastructure services to full-stack capabilities.

To sweeten their appeal, hyperscalers are offering next-generation services including artificial intelligence (AI), machine learning (ML), Internet of Things (IoT), natural language processing (NLP), augmented reality (AR) and virtual reality (VR), blockchain, and more. In addition, leading hyperscalers are evolving their operating models to attract enterprises, for example by adding financial and technical support, offering A-team talent for professional services, and providing deep resources for enterprise training.

However, enterprise willingness to engage not only with hyperscalers but also with non-hyperscalers indicates the strategic importance of private cloud, multicloud and traditional infrastructure in running their end-to-end enterprise IT landscape. Non-hyperscalers will continue to be relevant with enterprises often choosing non-hyperscalers for their unique capabilities.

These findings and more are shared in Everest Group's recently published report, "Cloud Hyperscalers: A Critical—But Not the Only—Building Block of Enterprise IT." This State of the Market report deep dives into the global IT cloud services market, providing data-driven perspectives on the market at large. The report evaluates cloud services trends and demand drivers, analyzes hyperscaler offerings, and describes how hyperscalers have moved beyond providing infrastructure services to now cater to the entire enterprise IT stack, making consuming technology easier.

**Enterprises also need non-hyperscale cloud vendors to run their digital businesses**

Enterprises believe hyperscalers have their sweet spots but other options are also needed to run their end-to-end enterprise IT landscape, according to Everest Group research. Non-hyperscale cloud vendors and IT service providers can capitalize on the advantages they have to offer enterprises, including the following:

- Innovative commercial models: Most non-hyperscale vendors have transformed their pricing models for on-premise deployments. This change has made enterprises reevaluate their infrastructure sourcing strategy and consider these vendors as an important and viable partner.

- Easier consumption models: Vendors have learned from cloud hyperscalers to make "as-a-service" consumption a key part of their strategy. Therefore, clients are open to the idea of a "local cloud" that can run independently or extend to form a hybrid edge-to-local distributed cloud architecture.

- Product innovation: Infrastructure vendors are bringing in innovative service offerings, not to compete with cloud hyperscalers but to demonstrate their capabilities to help clients in building a digital business. These innovations vary and include enterprise-grade security, workload-specific compute, single pane of management, and transparent invoicing. Some non-hyperscalers are also building "software only" platforms that are not tied to their infrastructure but can be deployed on any hosting environment to give flexibility to clients. In addition, many are significantly increasing open source adoption to not only reduce cost of solution but also provide a market standard offering.

- Enterprise context and consulting skills: Enterprise technology transformation projects are highly complex, require advanced consulting skills and need a combination of technical skills with vertical expertise. IT service providers have developed this skill set, whereas hyperscalers, comparatively, have a lesser understanding of the enterprise IT landscape.

- Deep industry knowledge: Service providers possess deep industry knowledge and better understand industry-specific challenges, allowing them to cater well to specific enterprise demands.

- Strategic client relationships: Service providers are viewed as trusted partners by enterprises. Their relationship over the years has witnessed multiple technology transformations. Service providers have proved their execution competency.

***Download a complimentary abstract of the report here.***

About Everest Group

Everest Group is a research firm focused on strategic IT, business services, engineering services, and sourcing. Our clients include leading global companies, service providers, and investors. Clients use our services to guide their journeys to achieve heightened operational and financial performance, accelerated value delivery, and high-impact business outcomes. Details and in-depth content are available at http://www.everestgrp.com

Media Contact

Andrea Riffle, Everest Group, 954-801-8474, [email protected]

Jennifer Fowler, Cathey Communications, 865-405-6380, [email protected]

SOURCE Everest Group

Share this article