Everest Group Says Two-Thirds of Enterprises Have Invested in Industry 4.0

As enterprises leverage emerging technologies for interconnectivity, digitalization and automation, outsourcing to service providers for industry 4.0 services grows steadily; majority of sourcing engagements involve IIoT, analytics, and AI/ML solutions.

DALLAS, May 24, 2021 /PRNewswire-PRWeb/ -- Industry 4.0 is where enterprises aim to be, with almost two-thirds already invested in some capacity. According to Everest Group, 34% of enterprises have invested in pilot projects and are evaluating returns; 24% have implemented use cases and are willing to scale up to enterprise-wide adoption levels; and 5% of enterprises are enjoying maturity in the digital domain and realizing significant gains across their businesses. The remainder of enterprises are either still in the strategy-building phase (14%) or early stages of adoption (23%).

Industry 4.0 is the latest phase in the industrial revolution, characterized by advanced themes of interconnectivity, digitalization, and automation, and made possible through technological developments in multiple fields, including Internet of Things (IoT), additive manufacturing, cloud computing, edge computing, analytics, robotics, cybersecurity, artificial intelligence (AI) and machine learning (ML).

In its recently released "Industry 4.0 State of the Market Report: A Transformational Leap in Cyber-physical Convergence," Everest Group analyses the global Industry 4.0 market, discusses the emerging trends among enterprises, and offers a detailed description of the outsourcing landscape for Industry 4.0 services.

Key findings:

The global Industry 4.0 market: The overall global spend for Industry 4.0 has been steady at approximately 15% over the past couple of years and stands at US$80-85 billion for calendar year 2019. The majority of growth can be attributed to the emerging areas of IoT, cloud, analytics and connected platforms.

Impact of COVID-19: Lack of visibility on returns and reduced cash flows have caused somewhat of a dip in enterprise spending on Industry 4.0 as a result of the pandemic; however, the change in workplace dynamics and remote work have only fueled the need to digitally enable factories and the workplace in the aftermath of COVID-19. Everest Group expects the market to recover well.

Top impediments to scaled adoption: Lack of management buy-in and organizational complexity remain key concerns when it comes to successful projects in this domain.

Emerging trends:

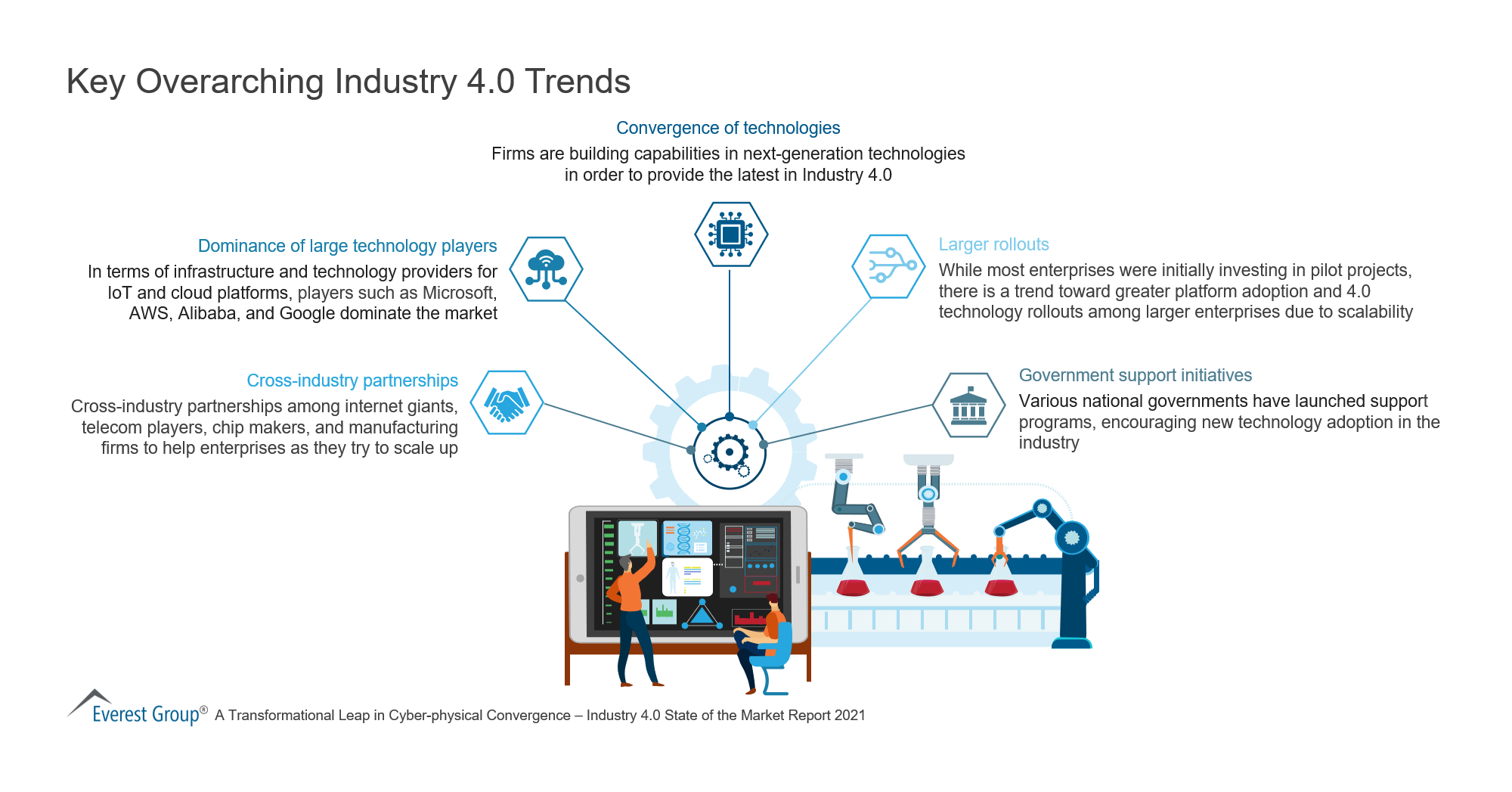

- Developing capabilities in multiple technology domains has become an imperative to delivering successful end-to-end solutions.

- Converging technologies within Industry 4.0 include 5G, cloud, analytics, connected systems, digital twins, mixed reality, robotics, intelligent assistants, additive manufacturing, nanotechnology, composite materials, AI and ML.

- Larger technology firms such as AWS, Microsoft and Google have dominated the industrial IoT market, with most others on the fringe.

- A number of government initiatives across the globe have been kickstarted to boost competitive advantage in emerging technologies. Examples include the U.S. government's "Advanced Manufacturing Partnership," Germany's "High Tech Strategy 2020," France's "La Nouvelle France Industrielle," China's "Made in China 2025," and South Korea's "Innovation in Manufacturing 3.0."

- Larger partnerships and rollouts are now becoming increasingly common as the market matures. For example, Microsoft and SAP announced a partnership to build Industry 4.0 solutions using existing cloud infrastructure and edge computing resources. Similarly, French automotive giant Renault has partnered with Google Cloud Platform to accelerate digitization of the supply chain and 22 facilities.

The role of service providers: Outsourcing spend for Industry 4.0 has experienced stable year-on-year growth over the last few years and captured roughly US$7.5 billion of the overall spend for calendar year 2019. Aerospace, energy and manufacturing-centric companies in North America, major automotive players in Germany, and industrial firms in the United Kingdom are the major contributors to this spend. Larger service providers hold the major portion of revenue; however, growth rate is higher among the smaller service providers. Service providers have invested in a range of competitive investments in order to expand the breadth and depth of their offerings; however, more than half of all customer engagements typically leverage only industrial IoT (IIoT), analytic solutions, and AI/ML solutions.

***Download a complimentary abstract of the report here.***

About Everest Group

Everest Group is a research firm focused on strategic IT, business services, engineering services, and sourcing. Our clients include leading global companies, service providers, and investors. Clients use our services to guide their journeys to achieve heightened operational and financial performance, accelerated value delivery, and high-impact business outcomes. Details and in-depth content are available at http://www.everestgrp.com

Media Contact

Andrea Riffle, Everest Group, 9548018474, [email protected]

Jennifer Fowler, Cathey Communications, 8654056380, [email protected]

SOURCE Everest Group

Share this article