National Taxpayer Advocate Reviews Filing Season and Identifies Priority Areas and Challenges in Mid-Year Report to Congress

(PRWEB) June 28, 2017 -- National Taxpayer Advocate Nina E. Olson today released her statutorily mandated mid-year report to Congress that presents a review of the 2017 Filing Season (FS), identifies priority issues the Taxpayer Advocate Service (TAS) will address during the upcoming fiscal year (FY), and contains the IRS’s responses to the 93 recommendations the Advocate made in her 2016 Annual Report to Congress.

Ms. Olson praises the IRS for a generally successful 2017 FS, including reducing the incidence of identity theft, implementing accelerated Form W-2 reporting requirements and matching Forms W-2 against tax returns claiming refunds. But Ms. Olson says taxpayers requiring assistance from the IRS still face significant challenges.

While taxpayer services and enforcement activities are essential for effective tax administration, Ms. Olson says taxpayer services require more emphasis than they currently receive. She points out that more than 60 percent of the IRS budget is allocated to enforcement activities while only about 4 percent is allocated for taxpayer outreach and education. Ms. Olson recommends that the IRS expand outreach and education activities and improve telephone services and that Congress provide the IRS with sufficient funding to provide high quality taxpayer service and conduct more oversight to ensure the IRS is spending funding as intended.

Overview of the Filing Season

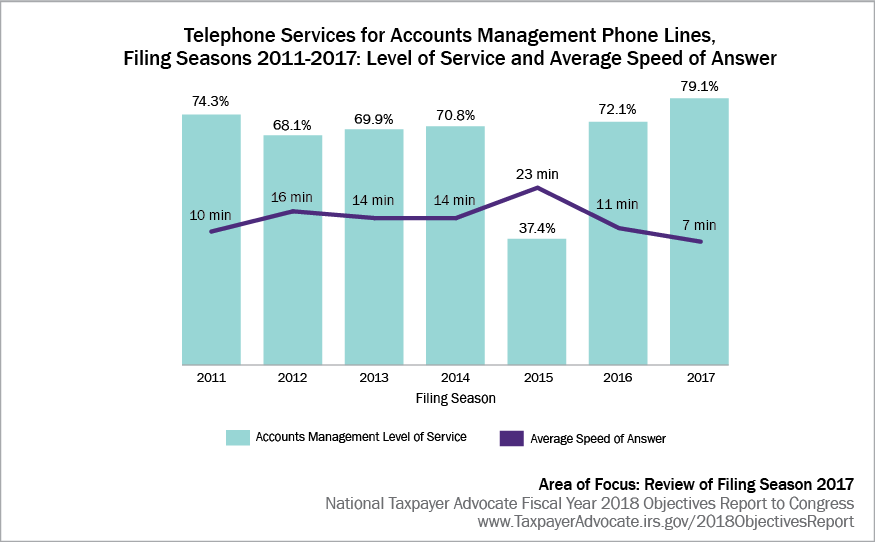

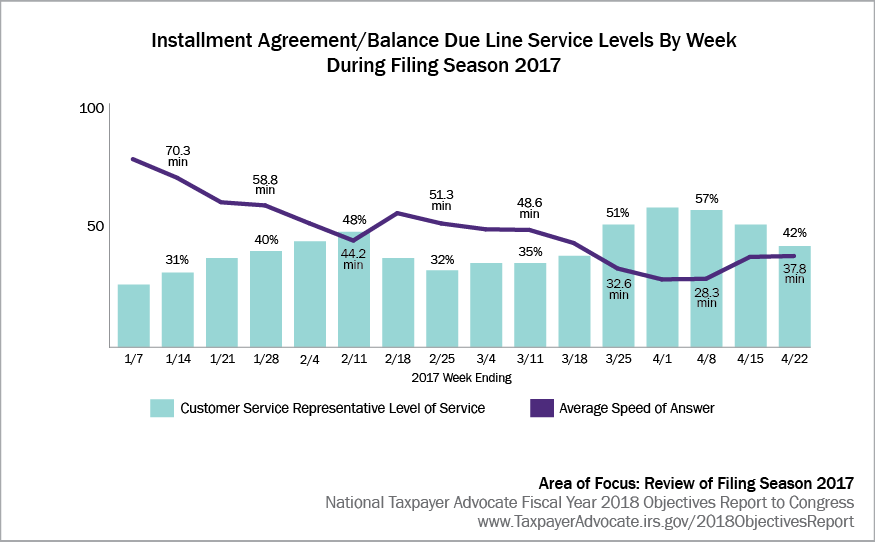

Overall, the IRS deserves credit for implementing multiple new legislative requirements related to the PATH Act. Taxpayers benefited from higher service levels and reduced wait times on many key phone lines.

However, much of the IRS’s improved performance is attributable to reduced taxpayer demand for services. While fewer taxpayers attempted to contact the IRS via telephone, the IRS also answered fewer calls. TAS remains concerned about the IRS’s recent and continuing reductions in taxpayer services, including declining to answer all but basic tax law questions during the FS or any questions after the FS, eliminating walk-in service at the TACs and eliminating taxpayer ability to ask the IRS questions online. The failure to meet the needs of taxpayers who rely on these services causes added stress for them and may reduce their willingness or ability to comply.

“To maintain and increase high voluntary compliance levels, it is imperative that the tax administrator make tax compliance as simple and painless as possible.”

Priority Issues for FY 2018

The report identifies and discusses 13 priority issues the Office of the Taxpayer Advocate will address during the upcoming FY, including:

Private Debt Collection (PDC) Implementation: In implementing its new PDC program, the IRS will disproportionately burden taxpayers in economic hardship. As of May 17, 2017, the IRS assigned to PCAs the debts of approximately 9,600 taxpayers, approximately 5,900 of whom filed a recent return. Returns show:

• These taxpayers’ median annual income is $31,689;

• More than half have incomes below 250 percent of the federal poverty level; and

• More than a fifth have incomes below the federal poverty level.

U.S. Passport Revocations and Denials: The IRS has broad discretion to exclude taxpayers from passport certification. However, the IRS chose not to exclude taxpayers with already open TAS cases who are actively working with TAS to resolve their tax problems. The IRS infringes on taxpayer rights by not notifying all affected taxpayers in a stand-alone notice before certifying their seriously delinquent tax debts.

Denials and Transparency in the Offshore Voluntary Disclosure Programs (OVDPs): Regarding the OVDPs, the IRS generally does not disclose its interpretations of the OVDP FAQs. It also withholds statistics that could help stakeholders evaluate the OVDPs and assure taxpayers they are not being treated unfairly. Disclosing FAQ interpretations and statistics could help reduce unnecessary calls, increase confidence in the IRS, reduce requests for advice and reduce unnecessary requests for assistance from TAS.

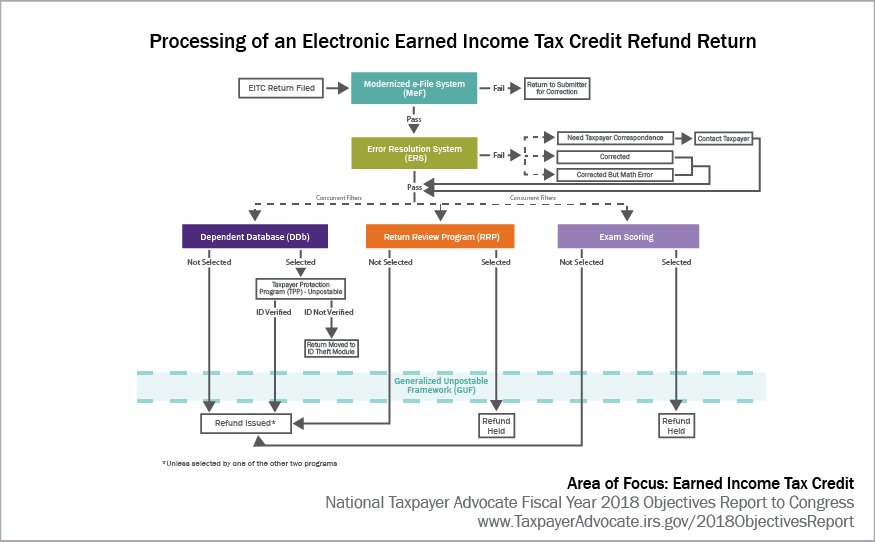

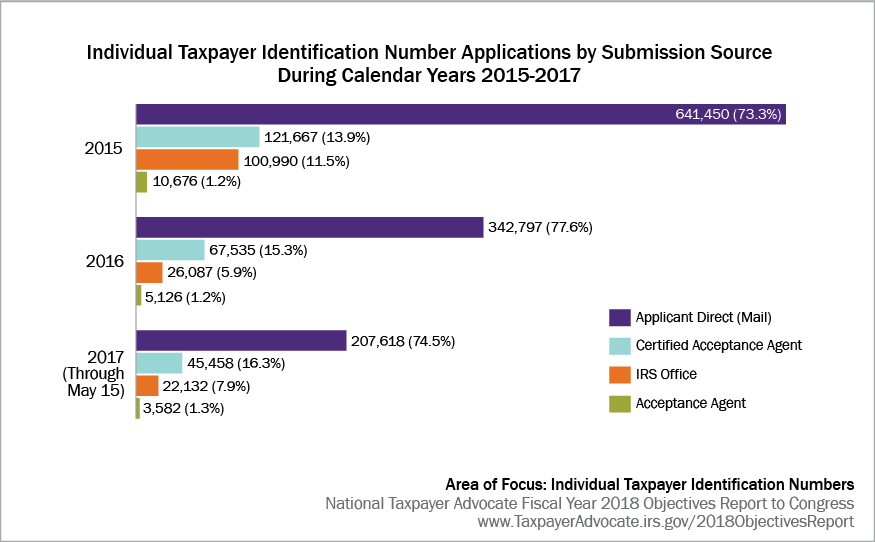

Other priority issues include the IRS’s approach to international tax administration; the advantages and disadvantages of the IRS’s emphasis on online taxpayer accounts; options to improve the EITC administration; tax compliance barriers for ITIN holders; the inadequacy of the IRS’s Allowable Living Expense standards; the IRS’s policies regarding levies on retirement accounts; the IRS’s efforts to combat tax-related identity theft; taxpayer challenges in complying with the Affordable Care Act; lack of specificity in third-party contact notices; and the IRS’s continuing information technology challenges.

Volume 2: IRS Responses to Taxpayer Advocate Recommendations

The National Taxpayer Advocate is required by statute to submit a year-end report to Congress that describes at least 20 of the most serious problems facing taxpayers and makes administrative recommendations to mitigate those problems. The report includes a second volume containing the IRS’s general responses to each of the problems the Advocate identified in her 2016 year-end report and specific responses to each recommendation. It also contains TAS’s analysis of the IRS’s responses and, at times, details TAS’s disagreement with the IRS’s position.

The Advocate made 93 administrative recommendations in her 2016 year-end report, and the IRS implemented or agreed to implement 35 of the recommendations, or 38 percent. Compared to last year, the IRS implemented or agreed to implement 65 of the 116 administrative recommendations proposed in the Advocate’s 2015 year-end report, or 56 percent.

“Both people who work in the field of tax administration and taxpayers generally can benefit greatly from reading the agency responses to our Annual Report in this Volume 2. Tax administration is a complex field with many trade-offs required. Reading both my office’s critique and IRS’s responses in combination will provide readers with a broader perspective on key issues, the IRS’s rationale for its policies and procedures, and alternative options TAS recommends.”

The National Taxpayer Advocate is required by statute to submit two annual reports to the House Committee on Ways and Means and the Senate Committee on Finance. The statute requires these reports to be submitted to the Committees without prior review or comment from the Commissioner of Internal Revenue, the Secretary of the Treasury, the IRS Oversight Board, any other officer or employee of the Department of the Treasury, or the Office of Management and Budget. The first report identifies the objectives of the Office of the Taxpayer Advocate for the FY beginning in that calendar year. The second report discusses 20 of the most serious taxpayer problems, identifies the ten most frequently litigated tax issues, and makes administrative and legislative recommendations to resolve taxpayer problems.

ABOUT THE TAXPAYER ADVOCATE SERVICE

The Taxpayer Advocate Service (TAS) is an independent organization within the IRS that can help protect your taxpayer rights. We can offer you help if your tax problem is causing a hardship or if you've tried but haven't been able to resolve your problem with the IRS. If you qualify for our assistance, which is always free, we will do everything possible to help you. Visit TaxpayerAdvocate.irs.gov or call 1-877-777-4778. For more information, go to TaxpayerAdvocate.irs.gov or irs.gov/advocate. You can get updates on tax topics at facebook.com/YourVoiceAtIRS, Twitter.com/YourVoiceatIRS, and YouTube.com/TASNTA.

Maryclaire Ramsey, Director, TAS Communications, Taxpayer Advocate Service, http://www.taxpayeradvocate.irs.gov/public-forums, (202) 317-6802, [email protected]

Share this article