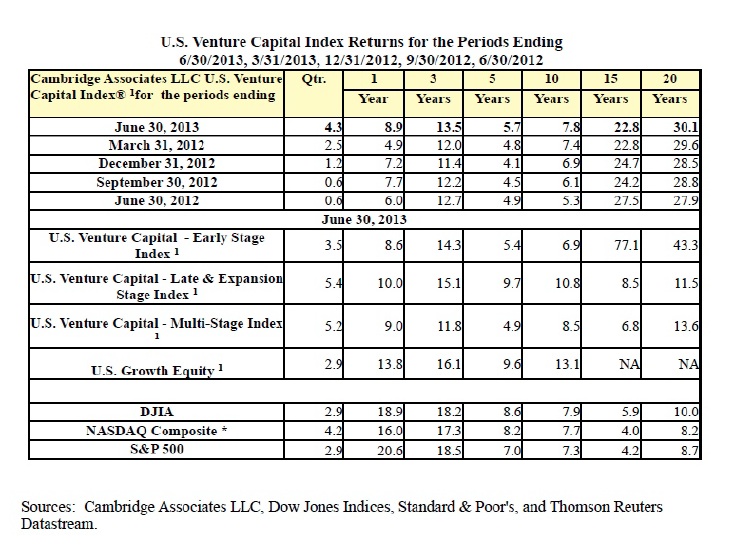

Venture Capital Fund Performance Strengthens Across Most Time Horizons

Arlington, VA (PRWEB) October 31, 2013 -- Venture capital performance improved significantly across nearly all time horizons as of June 30, 2013, according to the Cambridge Associates LLC U.S. Venture Capital Index®, the performance benchmark of the National Venture Capital Association (NVCA). Higher returns were seen in the quarterly, 1-, 3-, 5-, 10- and 20-year horizons with no change in the 15-year horizon. The 10-year performance continued its steady upward climb for the 13th consecutive quarter. The venture capital index outperformed the DJIA, NASDAQ Composite and S&P 500 across the quarterly, 15- and 20- year time horizons, falling short of these public indices in all other time periods.

In recognition of the increasing importance of the growth equity segment of the asset class, beginning with this quarter, the U.S. Venture Capital Index will include the aggregate performance benchmarks for U.S. growth equity funds.

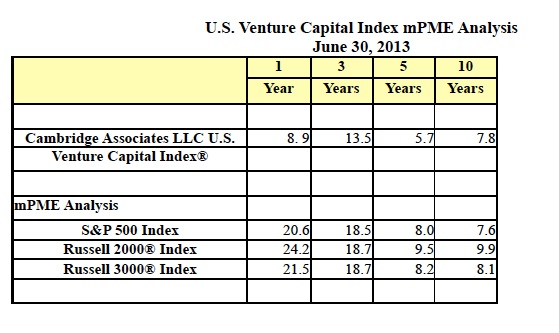

Cambridge Associates’ Modified Public Market Equivalent (mPME) 1 replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME NAV is a function of mPME cash flows and public index returns. “Value-Add” shows (in basis points) the difference between the actual private investment return and the mPME calculated return.

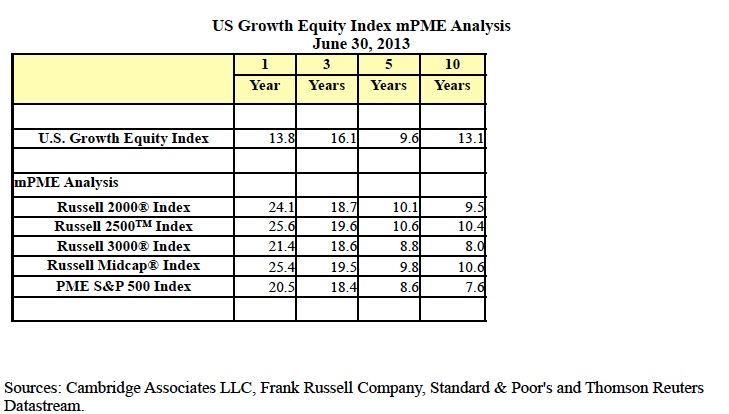

Cambridge Associates’ Modified Public Market Equivalent (mPME) 1 replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME NAV is a function of mPME cash flows and public index returns. “Value-Add” shows (in basis points) the difference between the actual private investment return and the mPME calculated return.

“Over long term time horizons greater than 15 years, U.S. venture capital has dramatically outperformed the public markets. With the benefit of hindsight, however, over the past decade it has been tougher for funds to outperform the public market alternatives. While we look to the public equity markets to provide good exit opportunities for current portfolios over the next few quarters, the focus by investors making commitments to future funds on likely top quartile funds going forward is understandable,” said John Taylor, head of research at NVCA.

“U.S. venture capital continued to show improved performance in the second quarter. The recent run-up in the public equity markets has eclipsed VC returns, contributing to underperformance relative to public market equivalent benchmarks in the 1-, 3- and 5-year periods. But it is important for investors to focus on the more meaningful long-term performance figures,” said Peter Mooradian, managing director and private investments research consultant at Cambridge Associates.

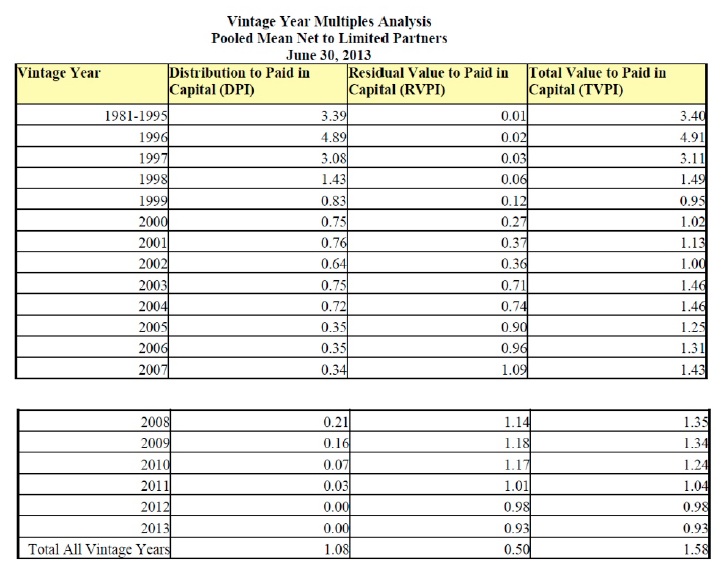

Vintage Year Return Ratios

The following chart lists the ratio between the dollars paid into venture capital funds by limited partners(LPs) and the dollars distributed to them by vintage year. For example, the 2002 vintage year funds have distributed cash of 0.64 times the amount of capital paid in by LPs and the residual value is 0.36 times the paid-in capital; the total value multiple is therefore 1.00 times. It is important to note that the residual value is unrealized and will change as companies exit the portfolio, are re-valued, or are written off. The 2003 and 2004 vintage year funds show the most positive ratio of the last decade, with each year returning 1.46 times the capital contributed by LPs, should those funds realize the value of what remains in the portfolio. More recent vintage years have yet to return significant cash to LPs as most funds do not have the opportunity to begin returning capital until after year five.

Additional Performance Benchmarks

To view the full, comprehensive report, which includes tables on additional time horizons, vintage years, and industry returns, please visit the Cambridge Associates or NVCA websites.

Cambridge Associates derives its U.S. venture capital benchmarks from the financial information contained in its proprietary database of venture capital funds. As of June 30, 2013, the database included 1,439 venture funds formed from 1981 through 2013.

About The National Venture Capital Association

Venture capitalists are committed to funding America’s most innovative entrepreneurs, working closely with them to transform breakthrough ideas into emerging growth companies that drive U.S. job creation and economic growth. As the voice of the U.S. venture capital community, the National Venture Capital Association (NVCA) empowers its members and the entrepreneurs they fund by advocating for policies that encourage innovation and reward long-term investment. As the venture community’s preeminent trade association, NVCA serves as the definitive resource for venture capital data and unites nearly 400 members through a full range of professional services. For more information about the NVCA, please visit http://www.nvca.org.

About Cambridge Associates

Founded in 1973, Cambridge Associates is a provider of independent investment advice and research to institutional investors and private clients worldwide. Today the firm serves over 950 global investors and delivers a range of services, including investment consulting, outsourced portfolio solutions, research services and tools (Research Navigatorsm and Benchmark Calculator), and performance monitoring, across asset classes. The firm compiles the performance results for over 5,400 private partnerships and their more than 68,000 portfolio company investments to publish its proprietary private investments benchmarks, of which the Cambridge Associates LLC U.S. Venture Capital Index® and Cambridge Associates LLC U.S.

Private Equity Index® are widely considered to be among the standard benchmark statistics for these asset classes. Cambridge Associates has been selected to provide data and to develop and maintain customized industry benchmarks for a number of prominent industry associations, including the Institutional Limited Partners Association (ILPA), Australian Private Equity & Venture Capital Association Limited (AVCAL); the African Venture Capital Association (AVCA); the Hong Kong Venture Capital and Private Equity Association (HKVCA); the Indian Private Equity and Venture Capital Association (IVCA); the New Zealand Private Equity & Venture Capital Association Inc. (NZVCA); the Asia Pacific Real Estate Association (APREA); and the National Venture Capital Association (NVCA). Cambridge also provides data and analysis to the Emerging Markets Private Equity Association (EMPEA). Cambridge Associates has more than 1,100 employees serving its client base globally and maintains offices in Arlington, VA; Boston; Dallas; Menlo Park, CA; London; Singapore; Sydney; and Beijing. Cambridge Associates consists of five global investment consulting affiliates that are all under common ownership and control. For more information about Cambridge Associates, please visit http://www.cambridgeassociates.com.

Channa Brooks, Tenor Communications for NVCA, NVCA, http://www.nvca.org, 202-812-6858, [email protected]

Share this article